After a car accident, medical providers often place liens on your settlement to guarantee payment for treatment. These auto lien medical bills can significantly reduce what you actually receive, and many people don’t understand how they work until it’s too late.

At Schaar & Silva LLP, we help injured people in Santa Cruz County, Sacramento, and Oakland navigate these complex financial obligations. This guide walks you through managing medical liens, negotiating costs, and avoiding costly mistakes that could impact your recovery.

What Happens to Your Medical Bills After an Auto Accident

Understanding Medical Liens and How They Work

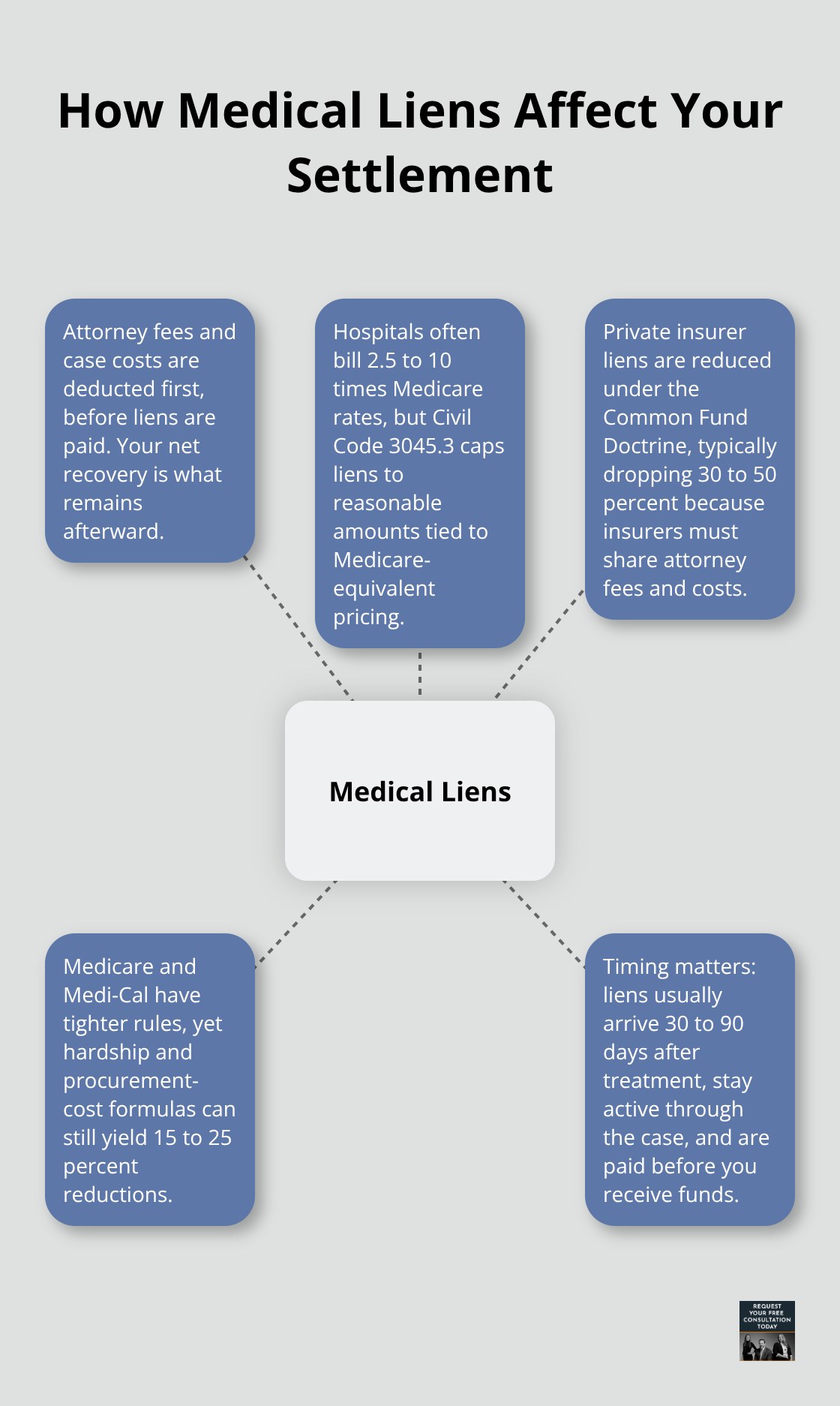

A medical lien is a legal claim that a healthcare provider places on your auto accident settlement to recover treatment costs they’ve already paid for. When you receive emergency care, surgery, or ongoing treatment after a crash, the provider doesn’t always demand payment upfront. Instead, they file a lien-a formal notice stating they’ll be paid directly from your settlement funds. This happens because accident victims often lack immediate cash to cover medical expenses, and providers know that settlements typically arrive months or years later. In California, providers can file liens even if you have health insurance, meaning the lien stacks on top of your existing coverage obligations. Hospitals file liens under California Civil Code 3045.2, which requires them to file within 20 days of learning about the injury. Missing that window makes the lien invalid, but most providers file quickly to protect their interests. Private health insurers and government programs like Medicare also use liens to recover what they’ve paid, though the rules differ for each type.

The Real Cost to Your Settlement

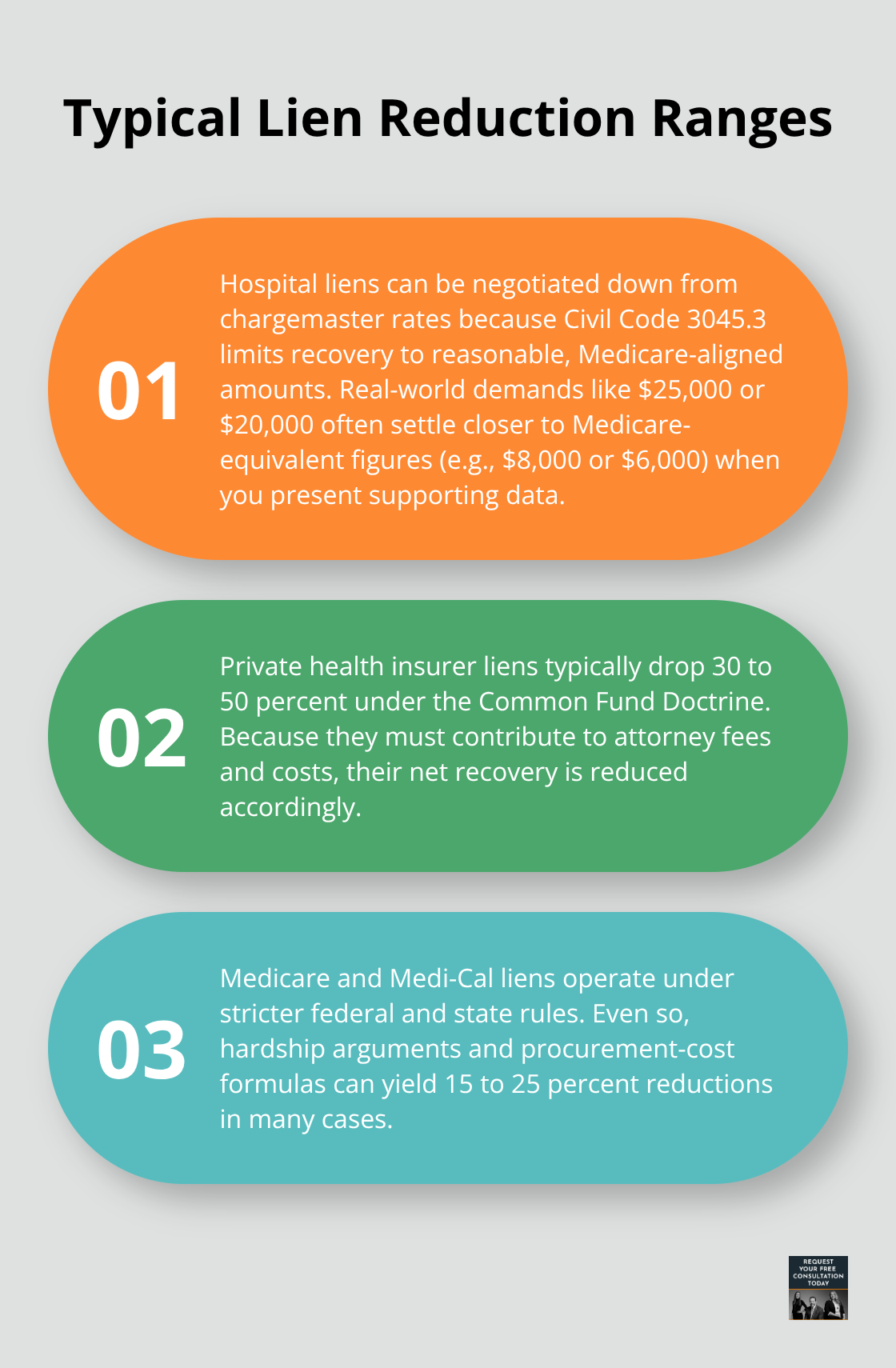

The financial impact is straightforward but often shocking. If your settlement reaches $100,000 and medical liens total $30,000, you don’t walk away with $70,000. Your attorney’s fees and costs come out first, then liens are paid, and you receive what remains. Hospital liens can be particularly aggressive because hospitals bill at chargemaster rates that run 2.5 to 10 times what Medicare pays for identical services. Under Civil Code 3045.3, hospital liens are capped at what the hospital would reasonably accept-essentially the Medicare rate for the same treatment. This creates significant negotiation leverage.

A hospital might demand $25,000 for surgery but accept $8,000 when presented with Medicare pricing. Private health insurer liens typically drop 30 to 50 percent through the Common Fund Doctrine, which requires lienholders to pay their proportional share of your attorney fees and costs. Medicare and Medi-Cal liens follow federal and state rules with tighter boundaries, making reductions harder but still possible through hardship arguments. Liens typically arrive within 30 to 90 days after treatment, remain active throughout your entire case, and are paid before you receive settlement funds.

Building Your Documentation Strategy

Start collecting expenses immediately after the accident. Gather itemized medical bills, dates of service, provider names, and records of all payments in a single file. Many medical bills contain duplicates, upcoding, or charges for services never rendered-error rates are high enough that thorough auditing strengthens your negotiating position. Create a running spreadsheet with dates, services, charges, and payments, updating it monthly. This organized approach prevents disputes and speeds reimbursement when working with a personal injury attorney. Medical treatment delays due to lack of upfront funds can worsen injuries and create gaps in medical records that undercut your claim value. Lien funding services available in Santa Cruz County and the surrounding areas can cover medical costs upfront, with repayment coming from your settlement later. This approach lets you access immediate care without depleting savings, maintain a strong medical record quickly, and avoid credit damage from unpaid bills. Pre-qualification typically takes about five minutes, and funds are paid directly to providers.

Taking Action on Medical Lien Services

Lien funding removes the financial barrier between you and the treatment you need. These services work by paying your medical providers directly while your case moves forward, ensuring you don’t face collection notices or credit damage during recovery. The process is simple: you qualify in minutes, funds reach your providers quickly, and repayment happens automatically from your settlement. This approach keeps your medical records complete and continuous, which strengthens your claim significantly. When you have gaps in treatment due to financial constraints, insurers and opposing counsel use those gaps to argue your injuries weren’t serious. Continuous care tells a different story-one that supports higher settlement values. Schaar & Silva LLP can direct you to medical lien services that work efficiently with your case, ensuring bills are paid without adding stress to your recovery process.

How to Negotiate Liens and Reduce What You Owe

Hospital Liens Offer the Biggest Savings Opportunity

Hospital liens represent your strongest negotiation position because hospitals charge 2.5 to 10 times Medicare rates for identical procedures. California Civil Code 3045.3 caps hospital liens at what the hospital would reasonably accept-essentially Medicare pricing becomes your negotiating floor. Request an itemized bill and compare each charge to the Medicare Physician Fee Schedule available through CMS. A hospital demanding $20,000 for emergency surgery might accept $6,000 when confronted with Medicare data showing that’s the standard reimbursement rate. This gap between chargemaster rates and actual Medicare payments creates substantial leverage in your favor.

Private Insurer and Government Program Liens

Private health insurer liens typically drop 30 to 50 percent through the Common Fund Doctrine, a legal principle requiring lienholders to contribute toward your attorney fees and costs. If your settlement reaches $80,000 with a $35,000 insurer lien and $20,000 in attorney fees, the insurer effectively pays roughly $8,750 of those fees, reducing their net recovery significantly. Medicare and Medi-Cal liens follow federal and state rules with tighter boundaries, but hardship arguments and procurement-cost formulas still yield 15 to 25 percent reductions in many cases.

Contact lienholders in writing with a settlement structure proposal addressing liens upfront rather than waiting until settlement closes. Early negotiation prevents last-minute disputes that delay your funds by weeks.

Audit Medical Bills for Errors and Duplicates

Start by auditing all medical bills for duplicates, upcoding, and charges for services never rendered. High error rates in medical billing mean you’ll almost always find reduction opportunities. Many providers accept 20 to 40 percent reductions when presented with clear settlement math and medical billing analysis. A lien-by-lien review identifies inaccurate charges before any payment leaves your hands. Request a lien payoff statement confirming exact amounts due after settlement, protecting against surprise claims later.

Maintain Continuous Medical Care During Negotiations

Working with lien funding services keeps your medical care uninterrupted while negotiations happen. Medical treatment gaps-missing imaging, skipped physical therapy sessions, delayed specialist visits-create ammunition for insurers to argue injuries weren’t serious. Continuous care tells the opposite story and strengthens settlement value significantly. Lien funding services in Santa Cruz County cover medical costs upfront, with repayment from your settlement, so you never face collection notices or credit damage during recovery. Pre-qualification takes about five minutes, and funds reach providers directly within days.

Know Your Rights and When to Hire Legal Help

Your rights as an injured party include controlling how medical information is shared-only disclose what’s necessary for lien processing under HIPAA rules. You can demand a lien payoff statement confirming exact amounts due after settlement. If liens become complex involving multiple providers, ERISA plans, or amounts exceeding settlement value, hire an attorney to handle negotiations. The legal team at Schaar & Silva LLP can coordinate with lien holders, spot billing errors, and apply Common Fund math to secure reductions that often offset attorney fees through savings alone. When multiple liens stack up or settlement discussions stall, professional negotiation transforms what looks like a $40,000 deduction into a $15,000 one-a difference that matters far more than the cost of legal help.

Mistakes That Drain Your Settlement

Question Lien Demands Instead of Accepting Them

Most injury victims accept medical bills and liens at face value without questioning whether the amounts are actually owed or negotiable. When a hospital sends a $25,000 lien demand, many people assume that figure is locked in stone. It isn’t. Under California Civil Code 3045.3, hospital liens are capped at reasonable amounts-essentially what Medicare or your insurer would pay for identical services. That $25,000 demand might settle for $8,000 when you present Medicare pricing data. The mistake happens because injured people focus on recovery, not paperwork. They sign documents without reading lien language, accept payment arrangements without understanding how liens interact with settlements, or worse, pay medical bills directly from their own pocket before a case resolves. Once you pay a bill out of pocket, you lose leverage to negotiate that lien later. Providers won’t reduce amounts you’ve already covered.

Audit Bills Before Settlement Discussions Begin

Documentation matters from day one. Collect every itemized bill, every provider statement, and every payment receipt immediately after the accident. High error rates in medical billing mean you’ll find duplicates, upcoding, or charges for services never rendered in nearly every bill set. A thorough audit before settlement discussions begin reveals reduction opportunities worth thousands of dollars. Many providers accept 20 to 40 percent reductions when you present clear evidence of billing errors or when settlement math shows the lien would leave you inadequately compensated. Request a lien payoff statement from every provider confirming exact amounts due. These statements prevent surprise collection notices weeks after you thought the case was closed.

Resolve Liens Before Accepting Settlement Offers

Settling your case before addressing liens creates financial disaster. Injured people grow impatient after months of treatment and negotiation. When an insurance adjuster offers $85,000, the instinct is to accept immediately. But if you have $40,000 in medical liens and $20,000 in attorney fees, your net recovery drops to $25,000-far below what you actually need for ongoing care and lost wages. California medical debt has a four-year statute of limitations, meaning providers can pursue collection years after settlement. Before you sign any settlement agreement, obtain written lien payoff statements from every provider confirming exact amounts due. Request these statements 30 to 60 days before your anticipated settlement date. Early negotiation prevents last-minute disputes that delay fund disbursement by weeks.

Maintain Continuous Medical Care to Strengthen Your Claim

Documentation gaps create serious vulnerability. Missing records from emergency care, imaging, or therapy sessions leave lien exposure unaddressed. Opposing counsel uses gaps to argue injuries weren’t serious, which suppresses settlement value. Continuous medical care, supported by lien funding services available in Santa Cruz County, keeps your records complete and strengthens your claim significantly. Lien funding covers medical costs upfront with repayment from settlement, eliminating the financial barrier that forces treatment delays. When you maintain uninterrupted treatment records, you build a compelling narrative about injury severity that translates directly into higher settlement offers.

Handle Complex Liens with Professional Negotiation

If liens are complex-involving multiple providers, ERISA plans, or amounts exceeding settlement value-professional negotiation becomes essential. The legal team at Schaar & Silva LLP handles these negotiations so you don’t face unexpected deductions after settlement closes. Skilled negotiators spot billing errors, apply Common Fund math to secure reductions, and coordinate with lien holders to prevent last-minute surprises. These efforts often yield savings that offset the cost of legal assistance through reduced lien amounts alone.

Final Thoughts

Liens are negotiable starting points, not final numbers. Hospital liens typically drop 40 to 70 percent when you present Medicare pricing data, while private insurer liens fall 30 to 50 percent through the Common Fund Doctrine. Even Medicare and Medi-Cal liens yield 15 to 25 percent reductions through hardship arguments, meaning the difference between accepting a lien demand and negotiating it can mean thousands of dollars in your pocket.

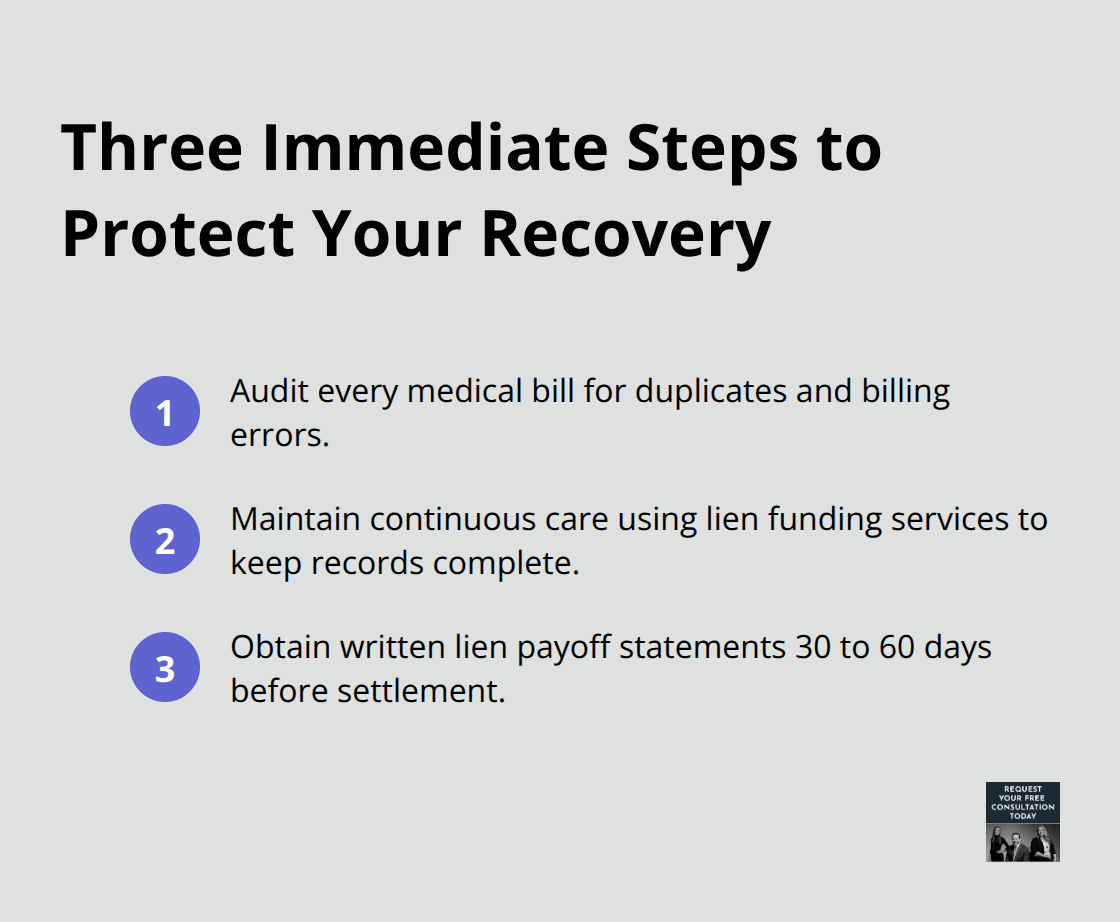

Three immediate steps protect your recovery from auto lien medical bills. Audit every medical bill for duplicates, upcoding, and billing errors before settlement discussions begin. Maintain continuous medical care using lien funding services available in Santa Cruz County so your treatment records remain complete and strong. Obtain written lien payoff statements from every provider 30 to 60 days before settlement to prevent last-minute surprises that delay your funds.

Contact Schaar & Silva LLP for a free consultation to review your lien situation, identify applicable California protections, and estimate realistic reductions. We direct you to medical lien services that cover bills upfront, coordinate with healthcare providers to reduce lien amounts, and handle complex negotiations so you don’t face unexpected deductions after settlement closes. You pay nothing unless recovery occurs.