A car crash claim involves more than just filing paperwork and hoping for the best. Insurance companies often undervalue claims, which is why knowing the right steps makes a real difference in what you receive.

At Schaar & Silva LLP, we’ve seen how proper documentation and strategic negotiation can significantly increase settlement amounts. This guide walks you through the process from the moment of impact to final compensation.

What to Do Right After a Crash

Move to Safety and Call for Help

The first hour after a car crash determines how strong your claim becomes. Most people freeze or make decisions they regret, but taking specific actions immediately protects both your health and your legal rights. Start by moving to safety if possible-if vehicles are drivable and there are no injuries, move them out of traffic to prevent additional crashes. Call 911 if anyone is injured or if there is significant damage; California law requires reporting any crash with injuries, deaths, or at least $1,000 in property damage to law enforcement according to the California Department of Insurance.

Document Everything at the Scene

At the scene, photograph everything before anything moves: the overall crash scene from multiple angles, all vehicle damage, the other driver’s license plate and vehicle identification number, road conditions, traffic signs, and any visible injuries. Take photos of the other driver’s insurance card and driver’s license. Collect the other driver’s full name, phone number, address, and email. Get the names and contact information of at least two witnesses-their statements become invaluable if the other driver later disputes what happened. Write down the police officer’s name and badge number along with the report number; if police do not attend, file an accident report with the California Department of Motor Vehicles within 10 days.

Protect Your Rights at the Scene and Beyond

Do not admit fault at the scene and do not discuss the accident with anyone except police and your own insurer. Contact your insurance company immediately, ideally within 24 hours. Provide factual information about what happened but do not give a recorded statement-tell the insurer you will provide a written statement after consulting with an attorney. Keep copies of the police report, all photos, medical records from any treatment at the scene or hospital, and receipts for any expenses related to the crash.

Seek Medical Attention and Preserve Evidence

Seek medical attention even if you feel fine; some injuries like whiplash or internal bleeding appear hours or days later, and medical records create an official timeline linking your injuries to the crash. The California Department of Insurance Consumer Hotline at 1-800-927-4357 provides guidance if you have questions about your rights or the claims process. Once you have documented the scene and sought treatment, the next critical phase involves gathering comprehensive evidence that strengthens your claim and demonstrates the full extent of your losses.

What Evidence Matters Most to Your Claim

Medical Records Create the Foundation

Medical records form the backbone of any car crash claim because they establish an official timeline linking your injuries directly to the crash. Obtain copies of all medical reports, test results, imaging studies, and treatment notes from every healthcare provider you visit-emergency room, hospital, urgent care, physical therapy, or your primary care doctor. The California Department of Insurance requires insurers to investigate within 15 days and respond within 15 days, which means your medical documentation must be complete and organized before you submit your formal claim. Request records immediately after treatment; delays in gathering documentation slow your settlement by weeks. Include receipts for all medical expenses, prescription costs, and medical equipment like braces or crutches. Photograph any visible injuries at the scene and document their progression over time with photos dated weekly-this visual evidence strengthens claims involving soft tissue injuries where medical imaging may show nothing but your pain is real and documented.

Property Damage Assessment Requires Independent Verification

Property damage assessment demands more than just an insurance estimate. Obtain repair quotes from at least two independent body shops, not just the insurer’s preferred shop; California law at Insurance Code Section 758.5 guarantees your right to choose your repair shop, and the insurer must pay reasonable costs per trade standards regardless of which shop you use. When you review repair invoices, verify whether replacement parts are original equipment manufacturer parts, reconditioned parts, or aftermarket parts-the invoice must identify this clearly. If the vehicle is declared a total loss, you receive the lesser of repair costs or actual cash value at the time of loss according to the California Department of Insurance.

Lost Wages and Expenses Require Meticulous Documentation

Lost wages and out-of-pocket expenses demand careful documentation to maximize your recovery. Collect pay stubs showing your regular income, written statements from your employer confirming lost work days and hourly rate, and receipts for every expense related to the crash (transportation to medical appointments, childcare costs while you recovered, home services you hired). Create a spreadsheet listing each expense with the date, amount, and description; this organized approach impresses insurers and prevents you from overlooking costs that accumulate quickly. When the insurer reviews your claim, this level of detail demonstrates that you took your recovery seriously and tracked every financial impact the crash caused.

Getting Insurance to Pay What Your Claim Is Actually Worth

Know Your Policy Before You Negotiate

Insurance companies count on you not knowing your policy inside and out. Pull out your actual policy document and read the coverage limits section carefully. Most California drivers carry liability coverage that pays for damage they cause to others, but your own medical bills and vehicle repairs come from collision coverage, comprehensive coverage, or uninsured motorist coverage depending on what happened. According to the California Department of Insurance, a typical claim payout equals the lesser of repair costs or actual cash value of your vehicle at the time of loss. You must know exactly what your policy covers and what limits apply before the insurer makes an offer.

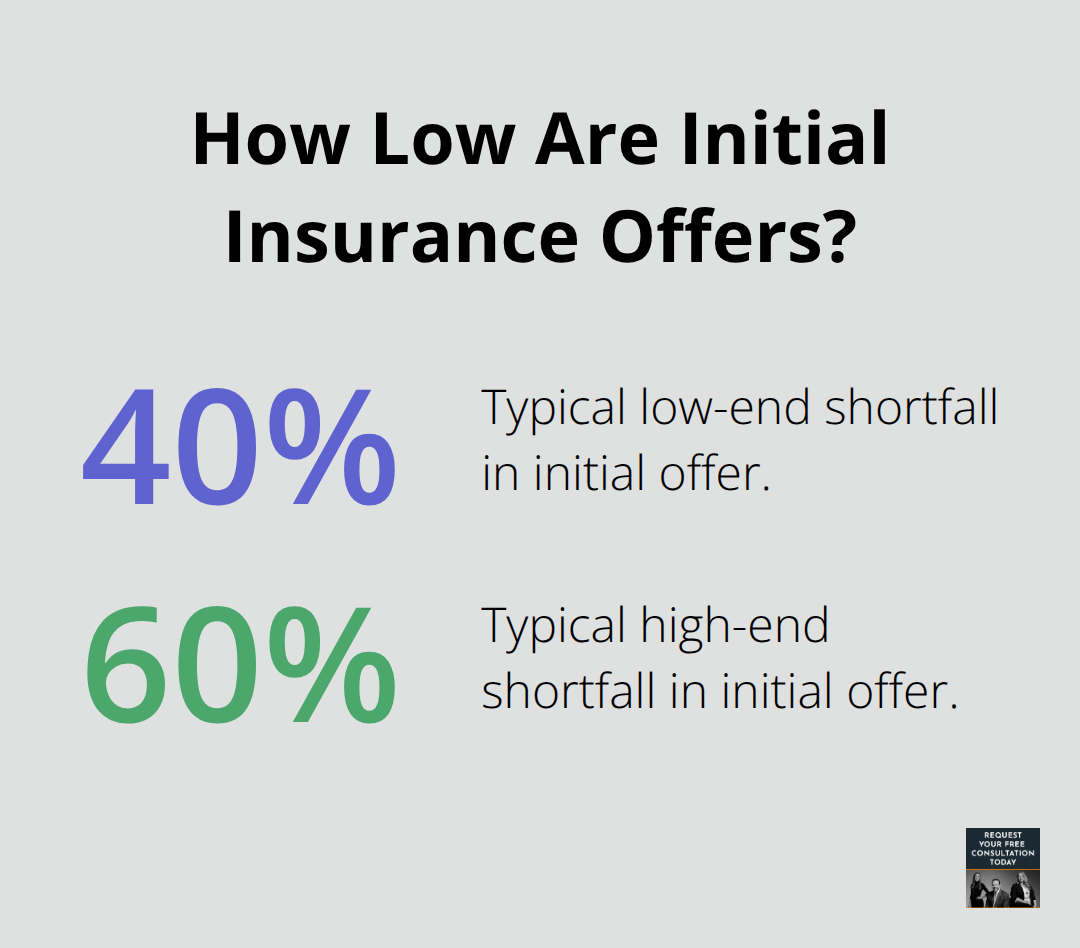

Reject Low Initial Offers with Evidence

When you call the insurer, do not accept the first number they suggest. Initial settlement offers routinely fall 40 to 60 percent below what claims actually settle for, and insurers bank on injured people accepting quickly out of desperation or confusion.

Present your evidence in a single organized document: medical records in chronological order, repair estimates from independent shops, wage loss documentation from your employer, receipts for every expense, and photos showing your injuries and damage progression. This professional presentation signals that you will not accept a lowball offer and that you have completed the work to prove your losses.

Push Back with Specific Numbers and Documentation

When the insurer responds with a settlement figure that does not match your documented losses, push back with specific numbers. If your medical treatment cost $8,500 and lost wages total $3,200 and vehicle repair estimates average $6,800, your minimum settlement before pain and suffering should be $18,500. California uses pure comparative negligence, which means even if you are partly at fault, you can still recover damages reduced only by your percentage of fault. If the insurer claims you are 20 percent at fault, your recovery is reduced by 20 percent, not eliminated entirely.

Monitor Insurer Timelines and Escalate When Necessary

The California Department of Insurance requires insurers to acknowledge claims within 15 days, respond within 15 days, and accept or deny within 40 days after you submit proof of claim. If your claim sits longer than these timelines without movement, the insurer is not following state regulations and you have grounds to escalate. Send all offers, counteroffers, and evidence through email so you have a written record that you can reference later. Phone calls leave no documentation, which weakens your position if disputes arise.

Use Appraisal to Challenge Vehicle Valuations

If the insurer refuses to budge beyond an amount that clearly undervalues your losses, that refusal signals the need for legal representation to pursue litigation or demand appraisal. Many policies include an appraisal provision where each side selects an appraiser and a neutral umpire decides the vehicle’s value, with the agreed amount becoming binding. This process prevents the insurer from having final say on what your vehicle is worth, and it often results in higher valuations than the insurer’s initial assessment.

Final Thoughts

Securing fair compensation after a car crash claim requires three actions: you must document everything at the scene, gather comprehensive evidence of your losses, and negotiate strategically with your insurance company. Photos of the crash scene, medical records linking your injuries to the accident, repair estimates from independent shops, and proof of lost wages form the foundation of any successful claim. When you present this evidence professionally and organized, insurers recognize that you understand your rights and will not accept lowball offers.

Your recovery process extends beyond the settlement check because medical treatment may continue for weeks or months, and some injuries reveal themselves slowly. You should keep all medical records, continue documenting expenses, and maintain communication with your insurer in writing so you have proof of every interaction. If the insurer refuses to move beyond an offer that does not match your documented losses, appraisal provisions in your policy give you a path to challenge their valuation without going to court.

We at Schaar & Silva LLP understand that navigating a car crash claim while recovering from injuries feels overwhelming, which is why we serve Santa Cruz County, Sacramento, and Oakland to help clients evaluate property damage and handle the legal complexities so you can focus on healing. Contact our team to discuss your claim and learn what fair compensation looks like in your situation.