An accident with an uninsured driver can leave you facing unexpected medical bills, vehicle damage, and uncertainty about how to recover. California law requires drivers to carry minimum liability insurance, yet thousands of uninsured motorists still hit the road each year.

We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland navigate these complicated situations. This guide walks you through your options and shows you how to protect yourself when facing an uninsured motorist in California.

What Uninsured Motorist Coverage Actually Covers

Why UM Coverage Matters in California

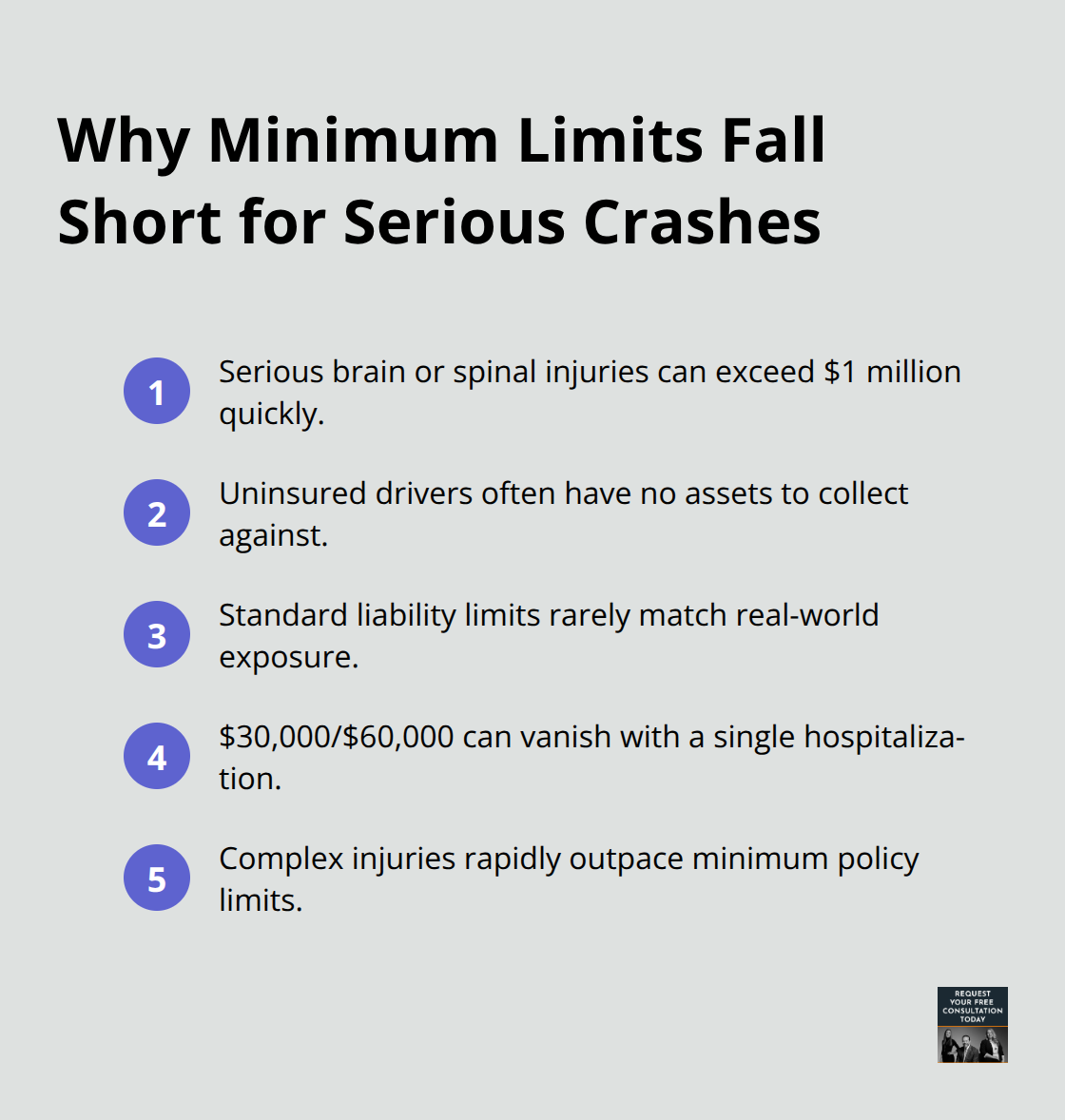

California requires all drivers to carry minimum liability insurance, yet about one in five drivers on California roads are uninsured according to the Insurance Research Council. This reality makes uninsured motorist coverage not optional-it’s a financial necessity. Uninsured motorist coverage, or UM, pays your medical bills, lost wages, and vehicle damage when the at-fault driver has no insurance. In 2025, California law requires insurers to offer UM coverage with minimums of $30,000 per person and $60,000 per accident for bodily injury, plus $15,000 for property damage. You can decline this coverage in writing, but doing so leaves you vulnerable to catastrophic financial loss.

The Real Cost of Serious Injuries

If an uninsured driver causes a brain injury or spinal cord injury-common in serious crashes-your damages can exceed $1 million. Without UM coverage, you would have to chase down an uninsured driver’s personal assets, which are often nonexistent. Most accident victims in Santa Cruz County, Sacramento, and Oakland carry standard liability limits that don’t match their actual exposure. A $30,000/$60,000 UM limit sounds reasonable until you face hospitalization with a serious injury.

Medical costs for brain injuries, spinal injuries, or multiple fractures quickly exceed these minimums.

Understanding Underinsured and Property Damage Coverage

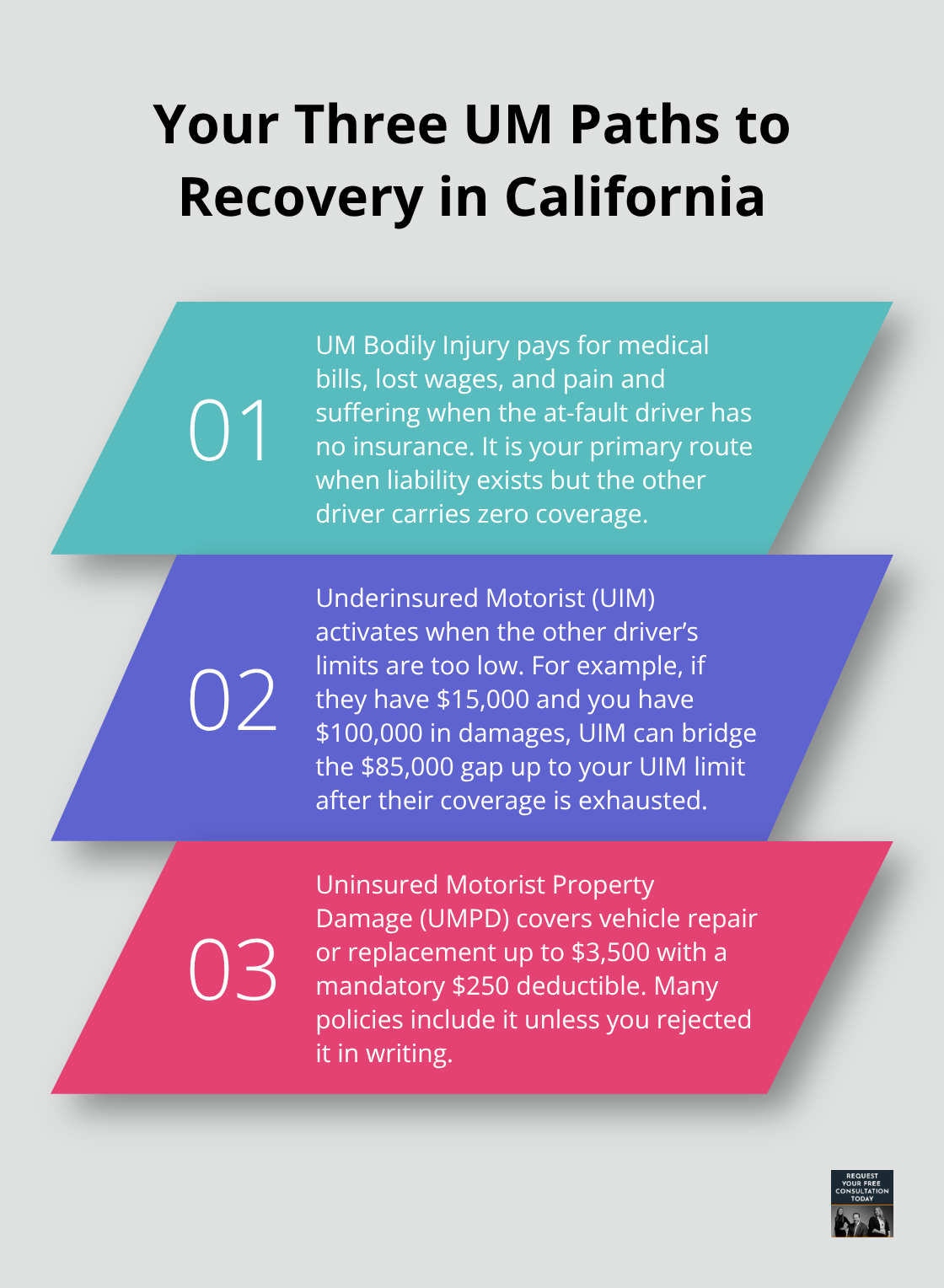

Underinsured motorist coverage, or UIM, works differently than UM. It covers you when the at-fault driver has insurance but their limits are too low to cover your actual damages. For example, if an underinsured driver with only $15,000 in coverage hits you and causes $80,000 in medical bills, your UIM coverage bridges that $65,000 gap up to your UIM limit. California also offers Uninsured Motorist Property Damage coverage, which covers vehicle damage from an uninsured driver up to $3,500 with a $250 mandatory deductible.

How Much Coverage You Actually Need

We recommend carrying at least $100,000/$300,000 in UM/UIM coverage, or $250,000/$500,000 if you have significant assets to protect. Higher limits cost only slightly more in premiums but provide genuine protection. Hit-and-run crashes are also covered under UM-California law requires proof of contact with the other vehicle, but once established, your UM coverage applies.

Taking Action on Your Policy

The key step is reviewing your current policy declarations page to see your actual UM/UIM limits, then discussing with your insurance agent whether those limits match your financial situation. Most people discover their coverage is inadequate only after an accident occurs. Once you understand what your policy covers, the next critical step is knowing exactly what to do if an uninsured driver hits you.

What to Do Immediately After an Uninsured Driver Hits You

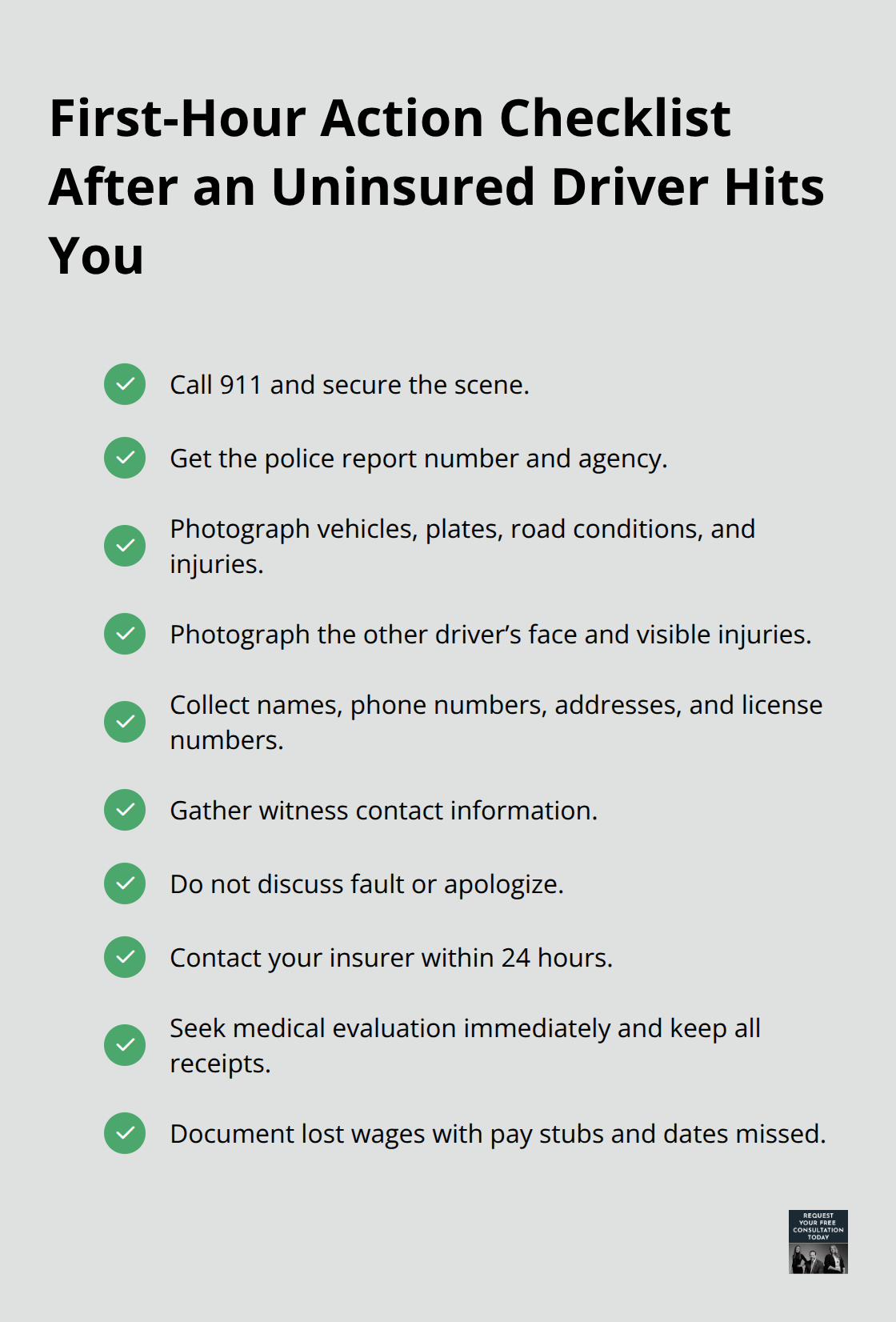

The moments after an accident determine whether you’ll have a strong claim or a weak one. California law requires you to report accidents causing injury or damage exceeding $750 to the Department of Motor Vehicles within ten days, but your real priority is what happens in the first hour.

Secure the Scene and Call for Help

Call 911 immediately if anyone is injured or if you feel unsafe moving your vehicle. Once emergency responders arrive, obtain the police report number and ask when the official California Highway Patrol or local police report will be available online-you’ll need this document for your insurance claim. While waiting for police, move to safety if possible and take photos of vehicle damage, the accident scene, road conditions, and the other driver’s license plate and vehicle. Photograph the other driver’s face and any visible injuries.

Collect Critical Information at the Scene

Get the names, phone numbers, addresses, and driver license numbers of all parties involved, plus contact information for any witnesses. Do not discuss fault, apologize, or make statements about injuries. Many people say things like “I’m fine” at the scene and later discover serious injuries; anything you say can be used against your claim later.

Contact Your Insurer and Seek Medical Care

Contact your insurance company within 24 hours-most policies require prompt notice, and delays can jeopardize your coverage. Tell your insurer you were hit by an uninsured driver and request a copy of your full policy, including the declarations page showing your UM/UIM limits and any arbitration provisions. Seek medical attention immediately, even if you feel okay. Whiplash, concussions, and internal injuries often appear hours or days after impact. Keep every medical receipt, prescription, and treatment note in one folder. Document lost wages by collecting pay stubs showing income lost due to medical appointments or recovery time.

Protect Your Claim Through Smart Communication

Do not give a recorded statement to your insurer without consulting an attorney-insurers use these statements to minimize payouts, and anything you say can limit your recovery. If the insurer pressures you for a statement, decline politely and say you’ll provide written responses instead. Report the accident to the California Department of Insurance if your insurer denies your claim or fails to contact you within 15 days. The California Department of Insurance maintains a complaint system that creates pressure on insurers to act fairly. Preserve all evidence by keeping originals of photos, medical records, police reports, and repair estimates in a safe place and back them up digitally. Do not post details about the accident on social media-insurers and opposing parties monitor these posts to find statements that contradict your claim.

Once you’ve taken these immediate steps and your insurer has received your claim, the formal claims process begins, and understanding how that process works will help you navigate what comes next.

How Your UM Claim Actually Works

Your insurance policy gives you three distinct paths to recover money after an uninsured driver hits you, and understanding which path applies to your situation determines how much you’ll receive. Uninsured motorist bodily injury coverage pays medical expenses, lost wages, and pain and suffering when the at-fault driver has zero insurance. Underinsured motorist coverage activates when the other driver has insurance but their limits fall short of your damages-if they carry only $15,000 in coverage and you have $100,000 in damages, your UIM bridges that $85,000 gap up to your UIM limit. Uninsured motorist property damage coverage handles vehicle repair or replacement up to $3,500, though you’ll pay a mandatory $250 deductible. The California Department of Insurance requires insurers to offer all three, and most policies include them unless you specifically rejected them in writing.

Verify Your Coverage Limits Today

Your declarations page lists your exact limits for each coverage type, so pull that document now and verify what you actually have. If your limits are lower than $100,000/$300,000, try raising them before your next renewal-the premium difference is minimal compared to the protection gap.

Understand the Claims Timeline

The claims timeline matters because California law gives you two years from the accident date to file a lawsuit, but your insurance policy may have shorter arbitration deadlines that are strictly enforced. After you notify your insurer of an uninsured driver claim, they typically investigate liability within 15 to 30 days, request medical records, and may hire an adjuster to inspect vehicle damage. Do not accept a settlement offer in the first month-insurers lowball initial offers knowing most people need cash quickly.

Calculate Your Actual Damages

Medical damages include all treatment costs from emergency room visits through ongoing physical therapy, prescription medications, and mental health counseling for accident-related trauma. Lost wage claims require pay stubs showing income lost during recovery and medical appointments, not estimates or rough calculations. Vehicle damage settlements are based on the lesser of repair costs or your vehicle’s actual cash value (the fair market price before the accident, not what you owe on a loan). If your car is totaled and you financed it, gap insurance covers the difference between the settlement and your loan balance-without it, you’re personally liable for that shortfall.

Get Help Evaluating Settlement Offers

We at Schaar & Silva LLP help accident victims in Santa Cruz County evaluate whether settlement offers from insurers fairly compensate your actual losses, and we push back aggressively when insurers undervalue claims.

Final Thoughts

An accident with an uninsured motorist in California creates immediate financial pressure and legal complexity that most people aren’t prepared to handle alone. One in five California drivers are uninsured, and your UM coverage is often the only protection standing between you and devastating personal liability. Protecting yourself starts now, before an accident happens-review your policy declarations page today and confirm your UM/UIM limits match your actual financial exposure.

After an accident occurs, the steps you take in the first hours determine whether your claim succeeds or fails. Call 911, document everything with photos, collect witness information, contact your insurer within 24 hours, and seek medical attention immediately. Do not give recorded statements without legal guidance, as insurers use these statements to minimize payouts and anything you say can permanently damage your recovery.

We at Schaar & Silva LLP help accident victims throughout Santa Cruz County, Sacramento, and Oakland navigate uninsured motorist claims and push back against insurers who undervalue damages. Contact us for a free consultation and let us handle the legal complexities while you focus on healing.