After a car crash, medical bills pile up fast. At Schaar & Silva LLP, we see clients struggle with these costs while their injury cases are still pending.

Car crash medical liens can help cover treatment expenses, but they come with real complications. Understanding your funding options now prevents costly mistakes later.

What Medical Liens Actually Take From Your Settlement

How Liens Reduce Your Recovery

A medical lien is a legal claim placed by hospitals, doctors, chiropractors, physical therapists, and other healthcare providers on your car accident settlement. When you receive treatment after a crash, these providers agree to wait for payment until your case resolves, but they secure that payment through a lien. The moment your settlement arrives, the lienholder gets paid directly from those funds before you see a dime. According to the Insurance Research Council, the average auto injury claim cost rose from $11,738 in 2005 to $15,506 in 2013, and those numbers have only climbed since.

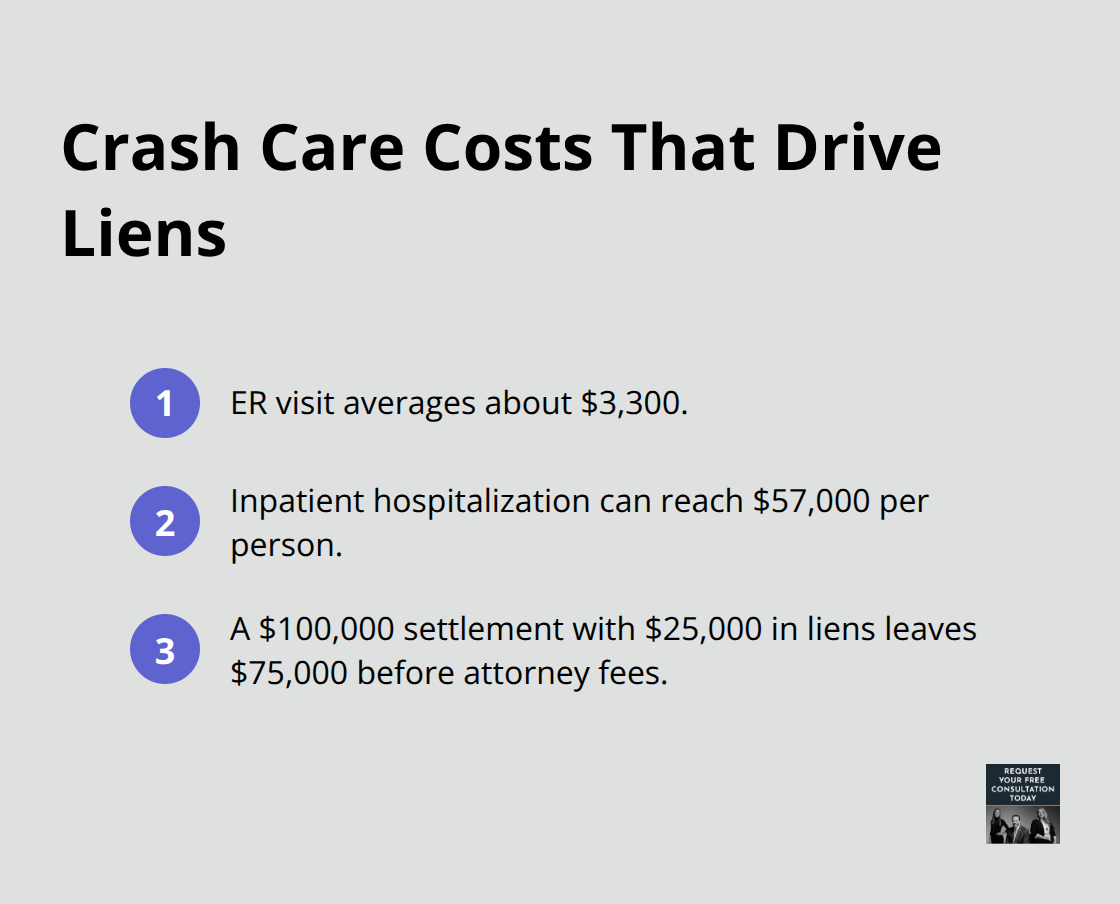

An emergency room visit for crash injuries runs about $3,300 on average, while inpatient hospitalization can reach $57,000 per person. These costs translate directly into lien amounts that reduce your net recovery dollar-for-dollar. A $100,000 settlement with $25,000 in liens leaves you with $75,000 before attorney fees and other deductions.

About 25% of auto-injury patients carry little to no health insurance, making medical liens the only realistic pathway to immediate treatment.

Why Providers Place Liens

Healthcare providers use liens to protect themselves from unpaid bills when injury victims lack insurance or when cases take months or years to settle. Government liens from Medicare or Medicaid follow stricter rules than private provider liens and are far harder to negotiate down. Missing a single lienholder creates serious problems: undisclosed liens resurface after settlement and can block your case closure.

Building Your Documentation Strategy

Documentation from day one is non-negotiable. Record every doctor visit, provider name, bill amount, date of service, and treatment type. Organize invoices and appointment cards into a dedicated file immediately. Before settlement, demand a written lien breakdown listing every lienholder, the exact amount claimed, and any negotiated reductions.

Negotiating Liens Down

Work with an attorney who identifies every lien early and negotiates reductions with providers to maximize what you actually receive. Many providers accept reduced amounts if you offer faster payment, and showing financial hardship strengthens your negotiating position. The team at Schaar & Silva LLP helps clients manage medical liens by directing them to medical lien services and ensuring no claims slip through the cracks during settlement.

Understanding these lien mechanics positions you to explore the specific funding options available while your case moves forward.

Your Funding Options During Treatment

Hospital and Provider Liens: The Default Path

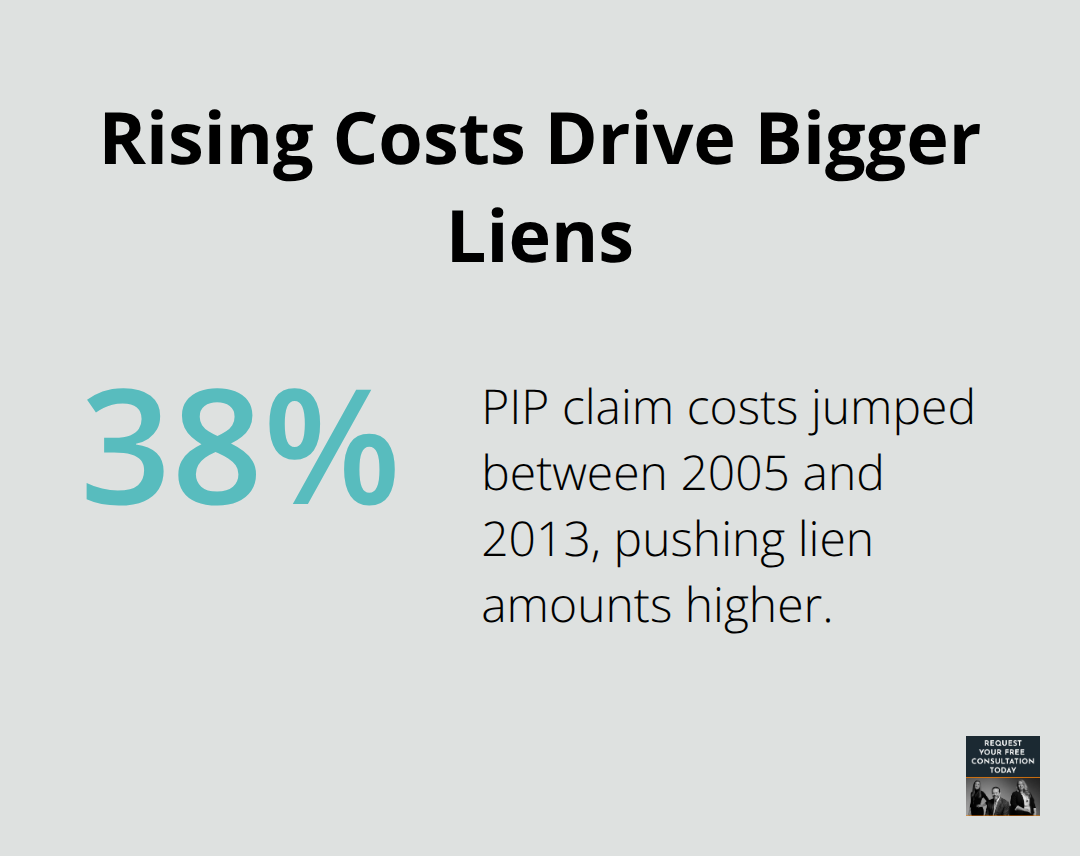

When medical bills arrive before your case settles, you face three distinct funding paths, each with different costs and timelines. Hospital and provider liens represent the most common approach: healthcare facilities treat you immediately and collect payment from your settlement later. This sounds convenient, but it carries real risks. Providers often bill at inflated rates and rarely negotiate without pressure. They hold the upper hand because they’ve already delivered care. The Insurance Research Council found that personal injury protection claim costs jumped 38% between 2005 and 2013, pushing medical lien amounts higher than ever. If you accept a hospital lien without review, you agree to whatever amount they claim, and that amount vanishes from your settlement dollar-for-dollar.

Government liens from Medicare or Medicaid operate under federal rules that make negotiation nearly impossible-these agencies rarely accept reductions and can place liens even after settlement if they weren’t properly identified beforehand.

Third-Party Medical Lien Companies: Speed and Structure

Third-party medical lien companies offer a different route. These firms advance money specifically to cover medical liens themselves. You apply, get approved quickly-often within hours-and receive funds within 24 hours after approval. The application takes about 5 minutes and requires no traditional credit check. This funding is non-recourse, meaning you repay only if you win or settle your case. If you lose, you owe nothing. Your attorney coordinates with the lender and deducts repayment from your settlement, so you keep whatever remains. Fund Capital America, which has operated since 2006, represents one established option in this space.

Pre-Settlement Funding: Broader Financial Relief

Pre-settlement funding operates similarly but covers broader expenses: medical bills, rent, utilities, groceries, transportation, and even vehicle repairs if your car was damaged. These advances don’t affect your credit score and carry no monthly payments. The catch is cost-funding companies charge interest or fees that reduce your net recovery, though this trade-off often makes sense when you’re facing eviction or can’t afford ongoing treatment. Compare offers from multiple lenders before committing; rates and terms vary significantly. Avoid any lender requiring upfront fees or promising guaranteed approval regardless of case strength. Strong case value determines eligibility, not your employment or financial history.

Choosing the Right Funding Strategy

Pre-settlement funding works best when you’re under time pressure to settle quickly; it gives you breathing room to negotiate liens properly and refuse unfair settlement offers. Each funding option carries trade-offs between speed, cost, and control over your settlement. Your next step involves understanding which lien reduction strategies actually work in practice and how to apply them to your specific situation.

Managing Liens Before Settlement

Document Every Medical Expense Immediately

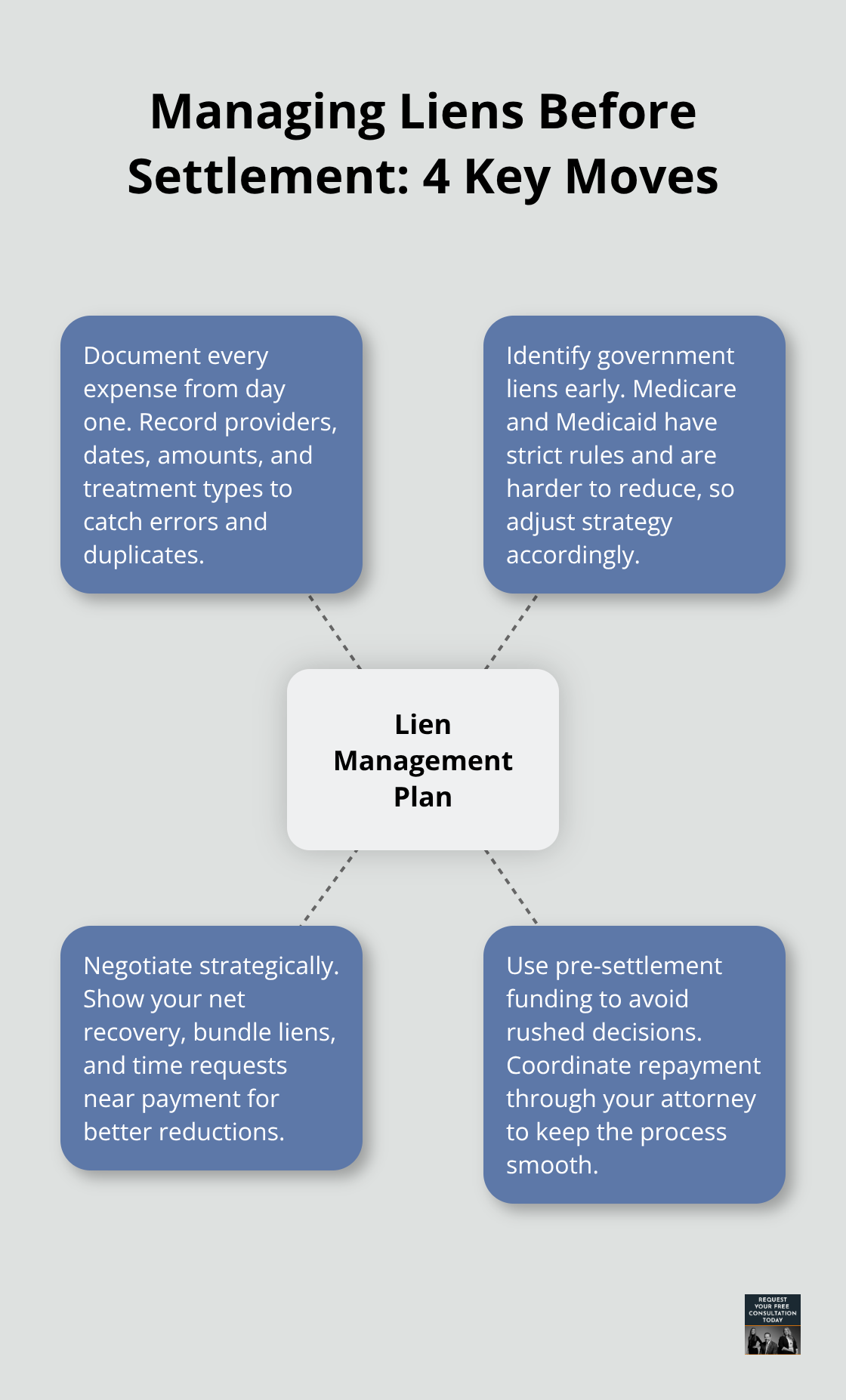

Start tracking medical expenses the day after your crash, not weeks later when bills arrive. Create a dedicated file and record the provider name, service date, amount billed, and treatment type for every visit. This documentation becomes your foundation for identifying duplicate charges, billing errors, and treatments unrelated to the accident. Many hospitals bill for services that have nothing to do with crash injuries, and if you don’t catch these errors early, you’ll lose money at settlement. Organize appointment cards, invoices, and provider contact information in one place so nothing gets lost.

Identify Government Liens Early

Request a written lien breakdown from your attorney before your case settles, listing every lienholder, the exact amount claimed, and which liens are government-related. Government liens from Medicare or Medicaid follow federal rules that make negotiation extremely difficult, so identifying these early changes your strategy entirely. Private provider liens, by contrast, respond to negotiation pressure because providers want payment and understand that unreasonable amounts can delay settlement. Your documentation creates an audit trail that proves which bills are valid and tied to crash injuries, giving you leverage when providers resist reductions.

Negotiate From a Position of Strength

Negotiation works best when you understand your settlement breakdown and can show providers exactly how much you’ll actually receive after attorney fees and other deductions. Many providers accept 30 to 50 percent reductions if you offer faster payment or demonstrate financial hardship from lost income and ongoing living expenses. Group multiple liens together and negotiate as a package rather than fighting each one separately, which saves time and gives you more negotiating power. Timing matters significantly: providers are most receptive to reductions when payment is imminent, not months away. Resolve every lien with documentation showing the final agreed amount before settlement to prevent surprises from unpaid claims.

Use Pre-Settlement Funding to Avoid Rushed Decisions

If your case involves substantial medical costs, pre-settlement funding can reduce time pressure to accept unfair terms. Funding gives you breathing room to negotiate properly instead of rushing to settlement because you need cash for rent or medical bills. This financial cushion allows you to hold firm on fair settlement amounts rather than accepting whatever gets offered quickly. Your attorney can coordinate with funding providers to ensure repayment happens smoothly from your settlement proceeds.

Final Thoughts

Medical liens after a car crash create real financial pressure, but you retain control over how much these liens ultimately cost you. Negotiating liens down directly protects your recovery, so start documenting medical expenses immediately and identify which liens come from government programs versus private providers. Pre-settlement funding removes the time pressure that forces rushed decisions, giving you room to negotiate properly instead of accepting whatever gets offered first.

Your next move depends on your specific situation and timeline. If medical bills are piling up and your case will take months to resolve, explore pre-settlement funding or medical lien company options to cover immediate expenses. If you’re closer to settlement, focus energy on negotiating lien reductions by showing providers your actual net recovery and offering faster payment in exchange for discounts (many providers accept 30 to 50 percent reductions when approached strategically).

Professional legal guidance matters because car crash medical liens involve complex rules, especially when government programs like Medicare or Medicaid are involved. At Schaar & Silva LLP, we help clients manage medical liens by directing them to appropriate services and ensuring no claims slip through the cracks during settlement. If you’re in Santa Cruz County, Sacramento, or Oakland and facing medical lien complications after a car or truck accident, contact us for a free review of your situation and settlement options.