Property damage claims in Oakland often leave homeowners frustrated and underpaid. Insurance companies use methods that don’t always reflect your actual repair costs, and low offers are common.

We at Schaar & Silva LLP help property owners understand their valuations, find fair repair quotes, and challenge inadequate settlements. This guide walks you through each step.

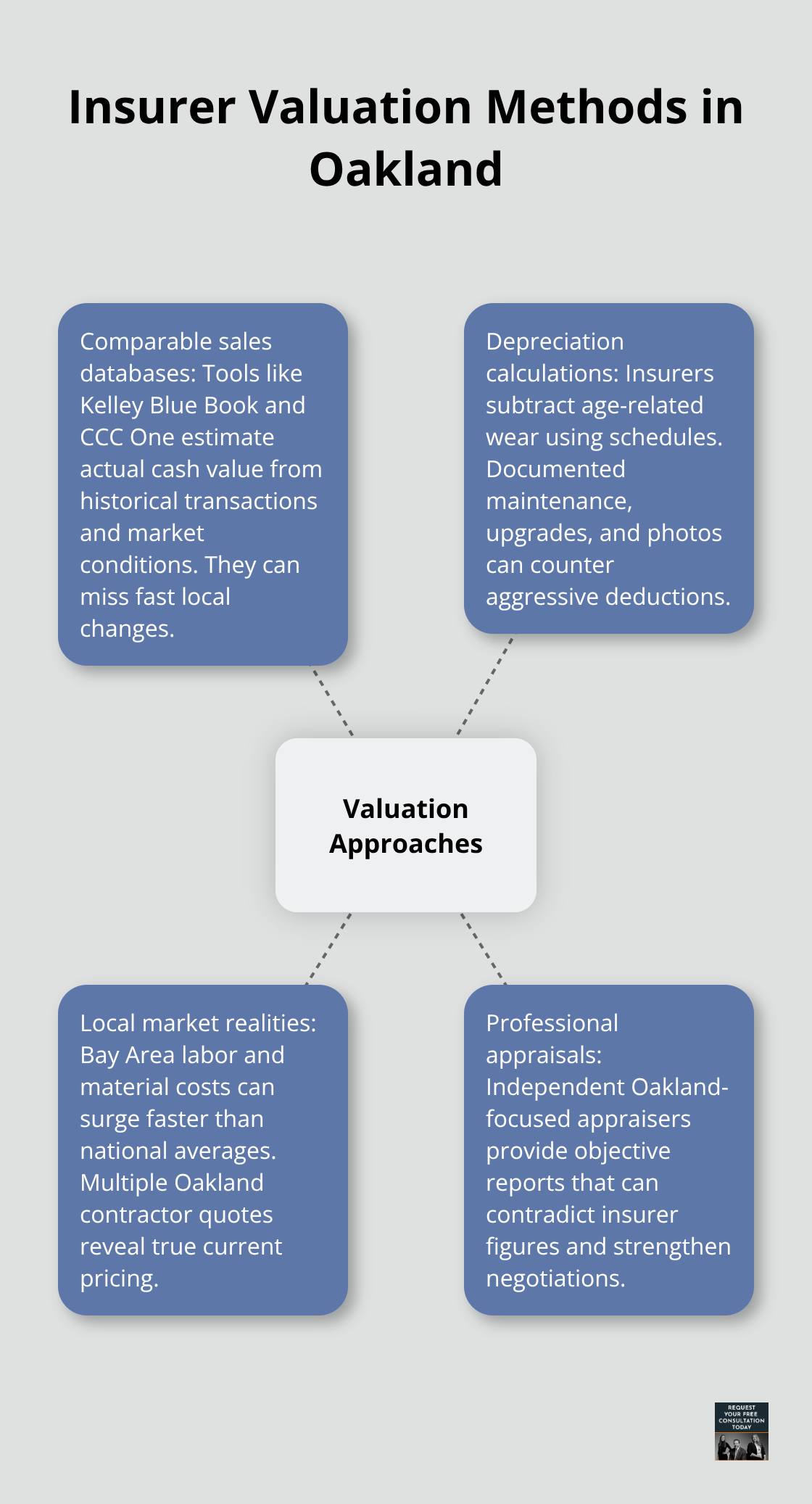

How Insurers Value Property Damage in Oakland

Insurance companies in Oakland rely on three primary valuation approaches, and understanding which one applies to your claim matters significantly. The most common method uses comparable sales data from Kelley Blue Book and CCC One, which pull historical transaction prices and current market conditions to establish actual cash value. However, these databases often lag behind local market shifts, meaning your property may be undervalued if Oakland’s repair costs have spiked recently.

California’s Comparable Sales Requirement

California law requires insurers to base calculations on two or more comparable sales sources, yet many adjusters rely too heavily on outdated national averages rather than Oakland-specific data. Your repair shop can provide a detailed estimate that challenges these generic figures, especially when your property has unique features or recent upgrades that don’t appear in standard valuations. Request a written explanation of the insurer’s comparable sales sources and demand they identify which specific Oakland properties or transactions support their figure. This forces transparency and often exposes reliance on properties that aren’t truly comparable to yours.

Depreciation: Where Disputes Arise Most Often

The second approach involves depreciation calculations, where insurers subtract age-related wear from the pre-damage value. This is where disputes arise most often because insurers apply blanket depreciation schedules that ignore your property’s actual condition or maintenance history. A well-maintained structure in Oakland’s competitive market often retains value better than the standard tables suggest, so documentation of repairs, upgrades, and upkeep becomes your strongest defense against aggressive depreciation. Photos and maintenance records directly counter the insurer’s assumptions about wear and tear.

Why Local Market Data Beats National Benchmarks

Oakland’s property market moves faster than national valuation tools can track. When repair costs surge due to labor shortages or material scarcity in the Bay Area, national databases don’t reflect those increases immediately. Gather multiple quotes from local Oakland contractors because their estimates reveal true current pricing in your area, not what a computer algorithm predicts. The salvage value component of the calculation also varies by location; Oakland’s recycling and parts markets differ from rural areas, affecting what an insurer claims your damaged property is worth as scrap.

Verifying Valuations with Professional Appraisals

Professional appraisers familiar with Oakland neighborhoods can verify whether the insurer’s valuation reflects genuine local conditions, and their independent assessment becomes powerful evidence if you need to challenge the offer later. An appraiser’s report that contradicts the insurer’s figure shifts the negotiation in your favor and demonstrates that you’ve invested in objective verification. If the insurer’s valuation seems disconnected from what local repair shops actually charge, that disconnect signals a problem worth investigating further. The next section covers how to find those trusted local repair shops and compare their quotes to identify fair pricing.

Where to Find Repair Shops That Won’t Lowball You

Selecting Specialized Contractors Over Generalists

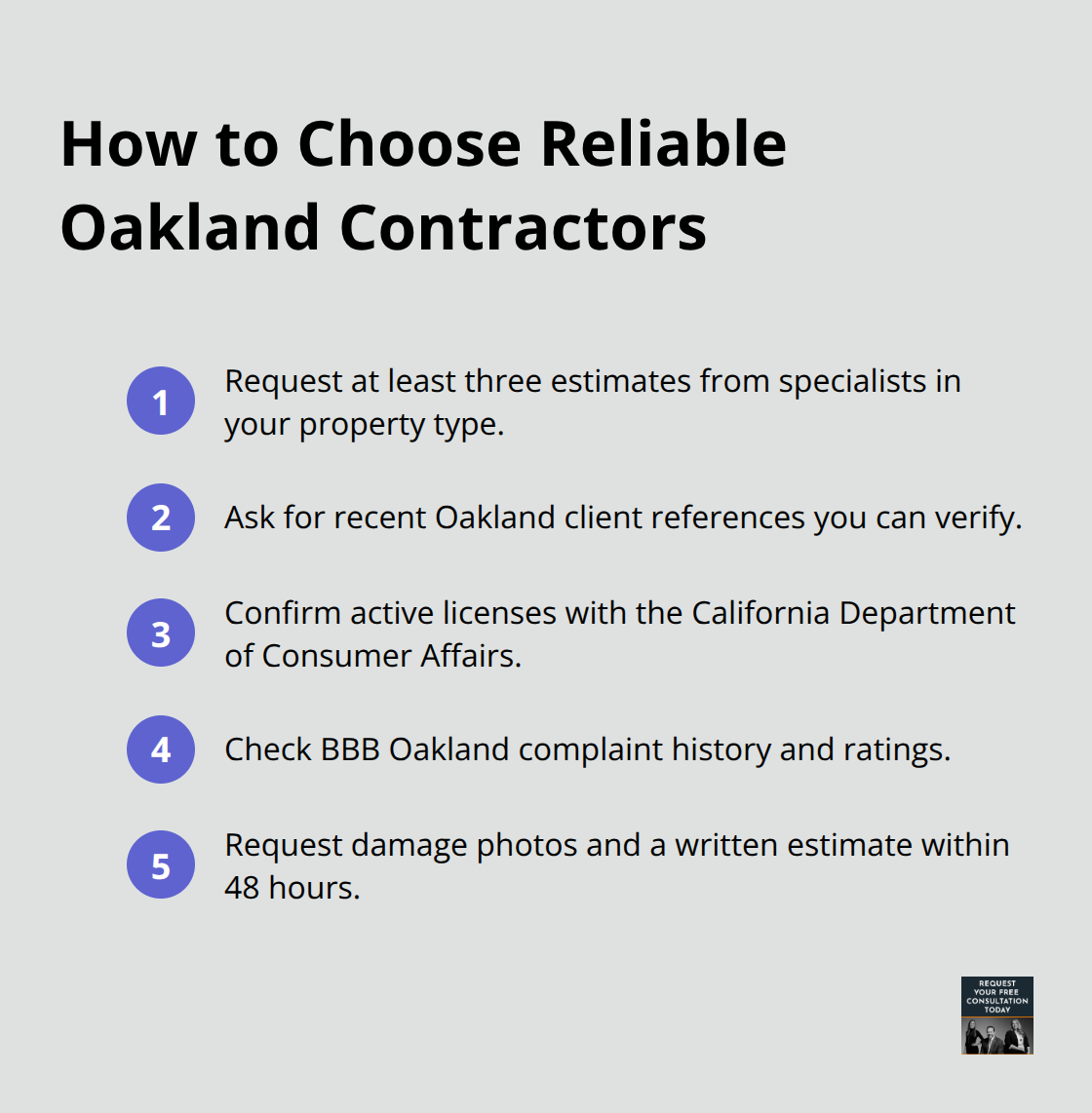

Oakland’s repair market varies significantly by neighborhood and contractor specialty, so the shop you choose directly affects whether your insurance settlement reflects actual repair costs. Start by requesting estimates from at least three contractors who specialize in your property type, not generalists who dabble in everything. Specialized contractors in Oakland typically charge 15–25% more than chain operations, but their detailed estimates become leverage when challenging the insurer’s valuation because they document exactly what needs fixing and why.

Ask each contractor for references from recent Oakland clients and verify they hold current licenses through the California Department of Consumer Affairs; unlicensed operators may quote low prices that disappear once work begins, leaving you liable for cost overruns that insurers won’t cover. Local trade associations like the Better Business Bureau Oakland branch maintain complaint histories, so check ratings before scheduling consultations. When contractors visit your property, request they photograph the damage and provide written estimates within 48 hours, not vague verbal quotes that change later.

Breaking Down Estimates Line by Line

Comparing estimates requires more than looking at the bottom number. Detailed estimates should itemize labor hours, material costs, and timeline separately so you can spot where contractors differ in their approach. If one quote is significantly lower than the others, ask that contractor specifically why-sometimes they use cheaper materials or plan shortcuts that compromise quality, and sometimes they’re simply hungry for work.

Oakland contractors familiar with insurance claims often include language about matching insurer requirements in their estimates, which signals they understand California’s building codes and won’t cut corners that create disputes later. This attention to detail protects you throughout the claims process.

Identifying Red Flags in Contractor Behavior

Red flags include contractors who pressure you to sign before you’ve reviewed the estimate with your insurer, those who quote prices that seem designed to match what you mention the insurer offered, or shops that discourage you from getting multiple quotes. Trustworthy contractors welcome comparison shopping because their pricing and methodology withstand scrutiny.

Once you’ve selected a shop, get a detailed scope of work in writing that specifies materials, labor, and completion timeline; this document becomes your standard against which the insurer’s offer is measured, and it protects you if the contractor’s costs increase mid-project. With solid repair estimates in hand, you’re positioned to negotiate your insurance settlement when any insurer valuation falls short of what local Oakland contractors actually charge for the work.

Disputing Low Insurance Offers and Maximizing Your Claim

Request Written Justification for the Insurer’s Valuation

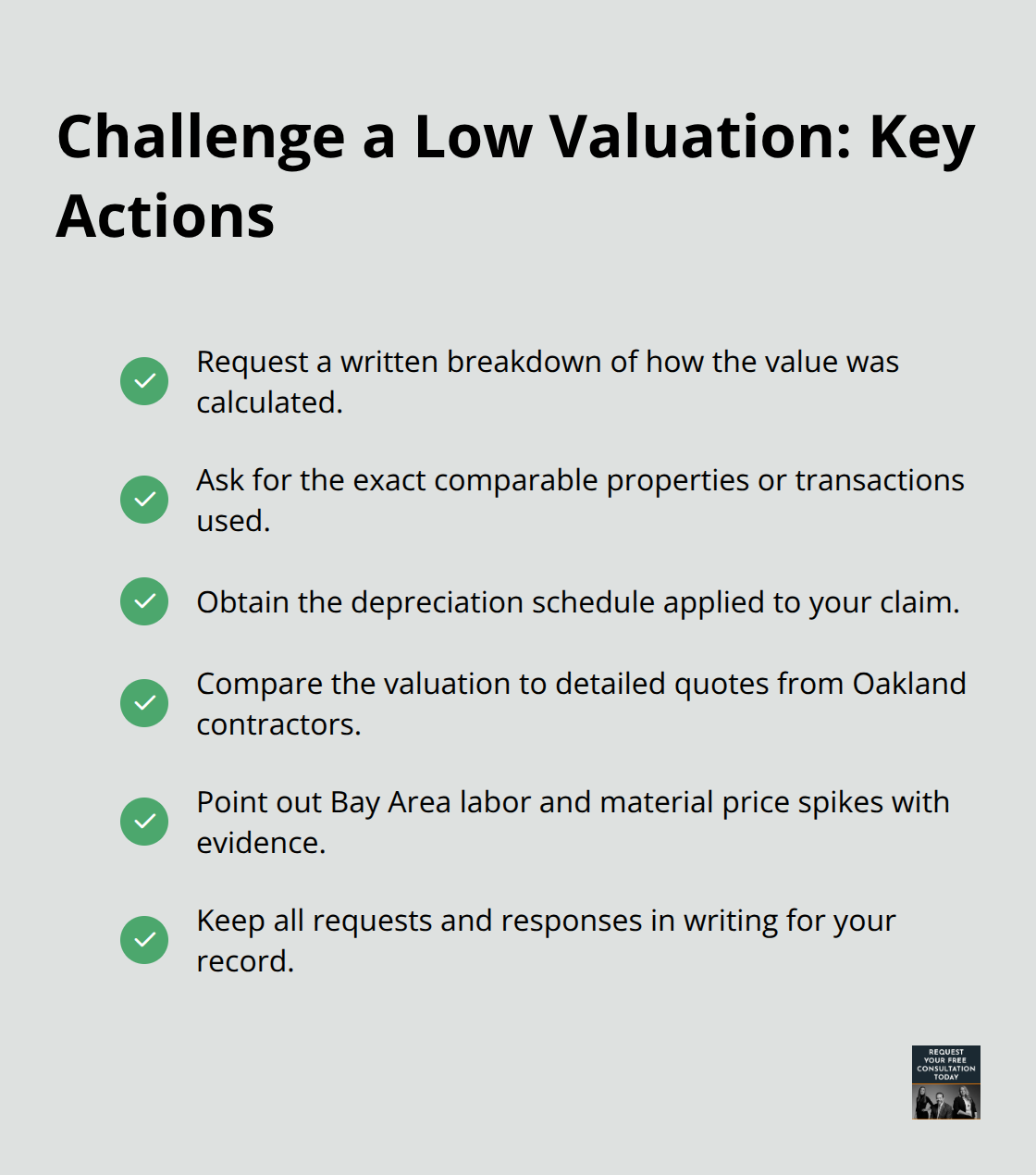

California Insurance Code § 790.03 requires insurers to investigate claims promptly and fairly, yet many Oakland property owners receive valuations that fall 20–40% below what local contractors actually charge for repairs. The gap exists because insurers use national databases that don’t capture Oakland’s current labor costs and material prices, which spike during Bay Area construction booms. When you receive a valuation from your insurer, request a written explanation of exactly how they calculated the figure, which comparable sales or properties they used, and what depreciation schedule they applied. California law mandates this transparency, and many insurers resist because their methodology won’t withstand scrutiny once you compare it to Oakland-specific data.

Identify Weaknesses in the Insurer’s Comparable Sales

Demand that the insurer identify the specific sources they relied on by name-Kelley Blue Book, CCC One, or whatever tool they used-and ask for copies of the comparable properties or transactions that support their number. If those comparables are from outside Oakland or are significantly different from your property in age, condition, or location, you’ve found your first leverage point. Request a reconsideration in writing, attaching the detailed estimates from the local contractors you consulted earlier and explaining precisely where the insurer’s valuation diverges from actual Oakland market conditions. Include photos showing your property’s pre-damage condition and any maintenance records that demonstrate it was well-kept, directly countering the insurer’s depreciation assumptions.

File a Complaint with the California Department of Insurance

The California Department of Insurance receives hundreds of complaints annually about undervalued property damage claims, and filing a formal complaint there adds pressure on the insurer to justify their offer or adjust it upward. This step costs nothing and creates an official record if you later pursue legal action. If the insurer refuses to adjust after reconsideration and your property damage claim exceeds several thousand dollars, the cost of an independent appraisal becomes justified.

Obtain an Independent Appraisal to Challenge the Insurer’s Figure

A licensed appraiser familiar with Oakland properties will conduct a thorough assessment and provide a report that directly contradicts the insurer’s figure if one exists. This report becomes your evidence in any subsequent negotiation or lawsuit, and many insurers increase their offers significantly once they see an independent professional assessment that contradicts their own. At this stage, consulting with an attorney who handles property damage disputes in California makes financial sense, especially if the insurer’s underpayment is substantial.

Pursue Legal Action for Bad-Faith Claims

We at Schaar & Silva LLP assist in evaluating the extent of property damage and ensure you receive a fair valuation for your loss. If negotiations fail, pursuing a bad-faith claim under California law is possible when an insurer has acted unreasonably or dishonestly, and successful claims can recover the unpaid balance plus interest, consequential damages, and in some cases attorney fees.

Final Thoughts

Property damage claims in Oakland require persistence, documentation, and a clear understanding of how insurers calculate valuations. The gap between what insurance companies offer and what local contractors actually charge for repairs is real, and it’s not accidental-insurers rely on national databases that lag behind Oakland’s current market conditions, depreciation schedules that ignore your property’s actual condition, and comparable sales data that may not reflect your neighborhood’s true costs. You have the power to challenge these figures by collecting detailed contractor estimates, requesting written justification from your insurer, and filing complaints with the California Department of Insurance when offers fall short.

Start with at least three estimates from specialized Oakland contractors who understand insurance claims and can itemize their work clearly. Compare these quotes line by line to identify fair pricing in your area, then use them as your benchmark when the insurer’s valuation arrives. Request written explanations of the insurer’s methodology, demand they identify their comparable sales sources by name, and reject vague references to national averages.

If the insurer refuses to adjust after reconsideration, an independent appraisal becomes your next step, especially for substantial losses. We at Schaar & Silva LLP help property owners navigate Oakland property damage claims by evaluating the extent of damage and ensuring you receive fair valuations for your losses. Contact us for a free case review to explore your options, including bad-faith claims and legal action.