A car accident in Santa Cruz can leave you facing mounting medical bills on top of physical pain and emotional stress. Medical expenses after a crash often exceed what insurance initially covers, leaving you responsible for the gap.

At Schaar & Silva LLP, we help accident victims understand how to use auto accident compensation to cover these costs. This guide walks you through the compensation available to you and practical steps to protect your financial recovery.

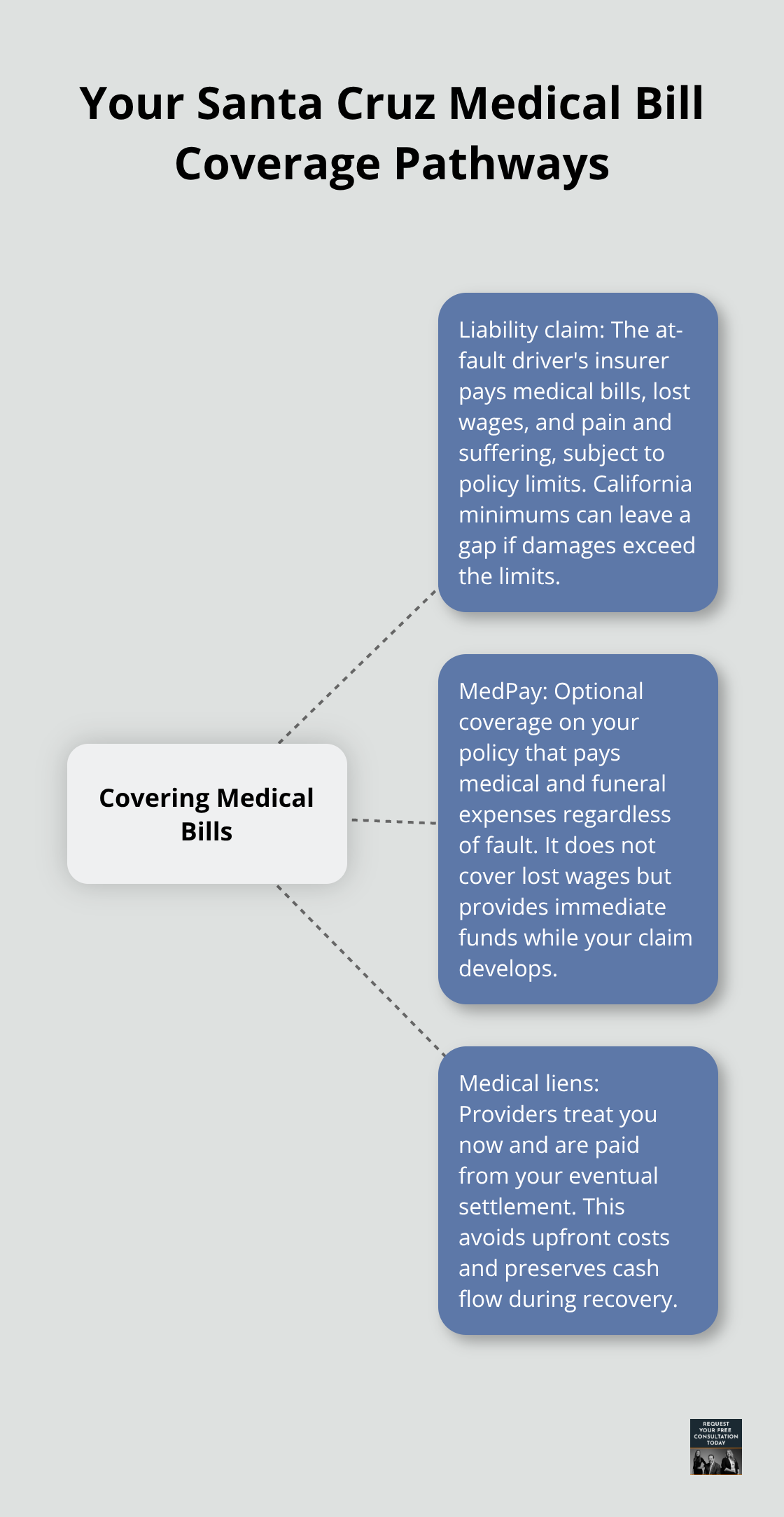

What Compensation Can You Actually Recover After a Santa Cruz Car Accident?

Liability Insurance: The Primary Source of Recovery

After a crash in Santa Cruz, the at-fault driver’s liability insurance must cover your medical bills, lost wages, and pain and suffering. California does not require no-fault personal injury protection, so you cannot rely on a mandatory PIP system like drivers in Florida or Michigan can. California’s minimum liability coverage is $30,000 per person and $60,000 per incident, according to California DMV Insurance Requirements. If the at-fault driver carries only these minimums and your damages exceed that amount, you face a significant gap. This limitation makes understanding your other compensation sources essential.

MedPay: Immediate Coverage Regardless of Fault

MedPay, an optional coverage you can add to your own policy, provides an immediate resource for medical bills regardless of fault. Unlike PIP, MedPay does not cover lost wages, but it covers medical expenses and funeral costs for you and your passengers. This distinction matters because medical bills arrive immediately after a crash while your personal injury claim develops over months. Reviewing your MedPay limits before you need them costs little and protects you substantially.

Comparative Negligence: Partial Fault Does Not Block Recovery

California’s pure comparative negligence rule allows you to recover damages even if you bear partial fault, but your settlement decreases proportionally. If you are found 20% at fault, your recovery drops by 20%. This rule creates leverage in negotiations because insurers cannot simply deny your claim based on partial fault. The at-fault driver’s insurer must still pay, making fault determination a negotiating point rather than a barrier to compensation.

Medical Liens: Securing Care Without Upfront Payment

Medical providers can file liens against your settlement to secure payment for services rendered, allowing you to receive care without upfront payment. This arrangement means your doctor gets paid from your eventual recovery, not from your pocket during treatment. Medical liens represent a compensation tool many Santa Cruz accident victims overlook, yet they unlock access to necessary care when cash flow is tight.

Understanding these three pathways-liability claims, MedPay, and medical liens-positions you to cover medical expenses strategically. The next section examines the specific medical costs that follow a crash and how to manage them effectively.

Managing Medical Bills After Your Santa Cruz Accident

Emergency and Specialist Costs Add Up Quickly

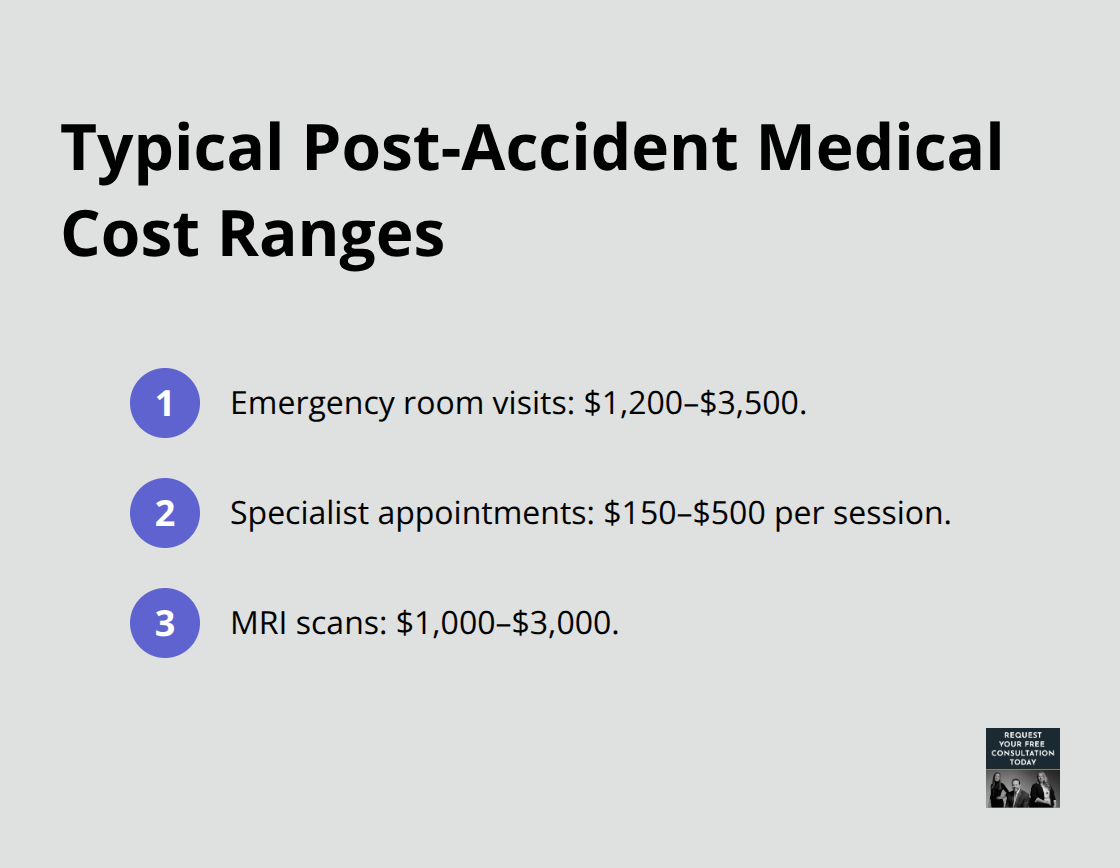

Medical bills after a car accident arrive in waves, and each one demands immediate attention. Emergency room visits typically cost $1,200 to $3,500 according to healthcare billing data, while follow-up specialist appointments run $150 to $500 per session. Physical therapy, often necessary after soft-tissue injuries, averages $60 to $150 per visit and may require 12 to 24 sessions over months.

If your accident caused fractures or required imaging like MRI scans, costs climb rapidly-MRI scans alone range from $1,000 to $3,000. The challenge intensifies because these bills arrive while you’re recovering and before your personal injury claim settles, which typically takes three to nine months for straightforward cases.

Medical Liens Free Up Your Cash During Recovery

Most accident victims don’t realize they can delay paying these bills through medical liens, a tool that lets providers wait for payment until your settlement concludes. A medical lien agreement directs your eventual settlement check to pay the healthcare provider first, then you receive the remainder. This arrangement matters because it prevents collection agencies from pursuing you while your claim develops, and it frees up your personal funds for living expenses during recovery. Santa Cruz providers routinely accept liens on personal injury claims, understanding that liability settlements eventually cover these costs.

Coordinate Your Coverage Sources Strategically

Navigating the overlap between your MedPay coverage, health insurance, and the at-fault driver’s liability claim requires a clear strategy. If you have MedPay with a $5,000 limit and health insurance with a $1,500 deductible, use MedPay to cover the deductible first, then let health insurance pay subsequent bills up to your MedPay limit. This coordination prevents you from depleting MedPay on costs health insurance should cover. Once MedPay runs out, file your liability claim against the at-fault driver’s insurer for remaining medical expenses. The at-fault driver’s insurer must reimburse your health insurance provider for any amounts they paid under what’s called subrogation-your insurer can recover what they paid from the liability settlement.

Document Everything and Request Future Cost Estimates

Document everything: collect itemized bills from each provider, request cost breakdowns, and maintain a spreadsheet tracking what each insurance source covers. Many accident victims miss out on full recovery because they fail to request written estimates for future care costs-if your doctor predicts you’ll need six months of physical therapy, get that estimate in writing and include it in your settlement demand. Out-of-pocket costs beyond medical bills add up fast: prescription copays, medical equipment, transportation to appointments, and lost wages while attending treatment. Track these expenses separately because they’re recoverable as economic damages.

Get Professional Guidance on Payment Arrangements

Coordinating these coverage sources and negotiating with providers about payment arrangements can feel overwhelming during recovery. We at Schaar & Silva LLP can help direct you to medical lien services that protect both your access to care and your financial recovery. Understanding how to leverage these tools positions you to move forward with your claim while your medical providers wait for payment from your eventual settlement.

How to Document Medical Costs and Recover Everything You’re Owed

Track Every Medical Expense Systematically

The moment you receive treatment after your accident, start tracking medical expenses. Create a spreadsheet with columns for the date of service, provider name, service type, billed amount, what insurance paid, what you paid out-of-pocket, and whether a medical lien was filed. This system prevents bills from falling through the cracks and gives you a complete picture of your actual costs versus what insurance covered. Many Santa Cruz accident victims lose thousands in recoverable expenses because they fail to track bills systematically.

Request itemized bills from every provider, not summaries, because itemized statements show exactly what you’re paying for and reveal billing errors. Healthcare billing mistakes happen frequently, and catching them early means you don’t overpay and don’t claim inflated amounts in your settlement demand, which insurers will challenge.

Establish Medical Liens Before Treatment Escalates

Within two weeks of your accident, contact each medical provider’s billing department and ask about their medical lien policies. Most Santa Cruz providers accept liens on personal injury claims without hesitation, and knowing this upfront lets you schedule necessary treatment without worrying about immediate payment.

Request written cost estimates for ongoing care from your treating physicians. If your doctor predicts you’ll need physical therapy twice weekly for three months, get that estimate on letterhead with the provider’s signature. These projections become powerful evidence in settlement negotiations because they’re your doctor’s professional assessment, not your speculation.

Capture All Out-of-Pocket Costs

Track every out-of-pocket expense beyond medical bills: prescription copays typically run $10 to $50 per medication, medical equipment like crutches or braces costs $50 to $300, transportation to appointments adds up if you need rideshare services, and lost wages during treatment days are fully recoverable. Many accident victims forget to claim these smaller expenses, but they compound quickly. If you missed five work days at $150 per day due to medical appointments, that’s $750 in recoverable wages you might otherwise overlook.

Negotiate Payment Arrangements Before Collections

Work directly with your medical providers on payment arrangements before bills reach collection. Call the billing departments and explain you’re pursuing a personal injury claim and ask about medical lien options or payment plans. Providers understand that accident victims face cash flow pressure during recovery, and most will work with you rather than send bills to collections. If a provider won’t accept a lien, ask about extended payment plans with zero interest. Some providers offer 12-month or 24-month payment plans that cost nothing extra, giving you time for your settlement to arrive. Never ignore medical bills or let them go to collections because that damages your credit and gives insurers ammunition to argue you’re not serious about your recovery.

Calculate Your Net Recovery After Settlement Obligations

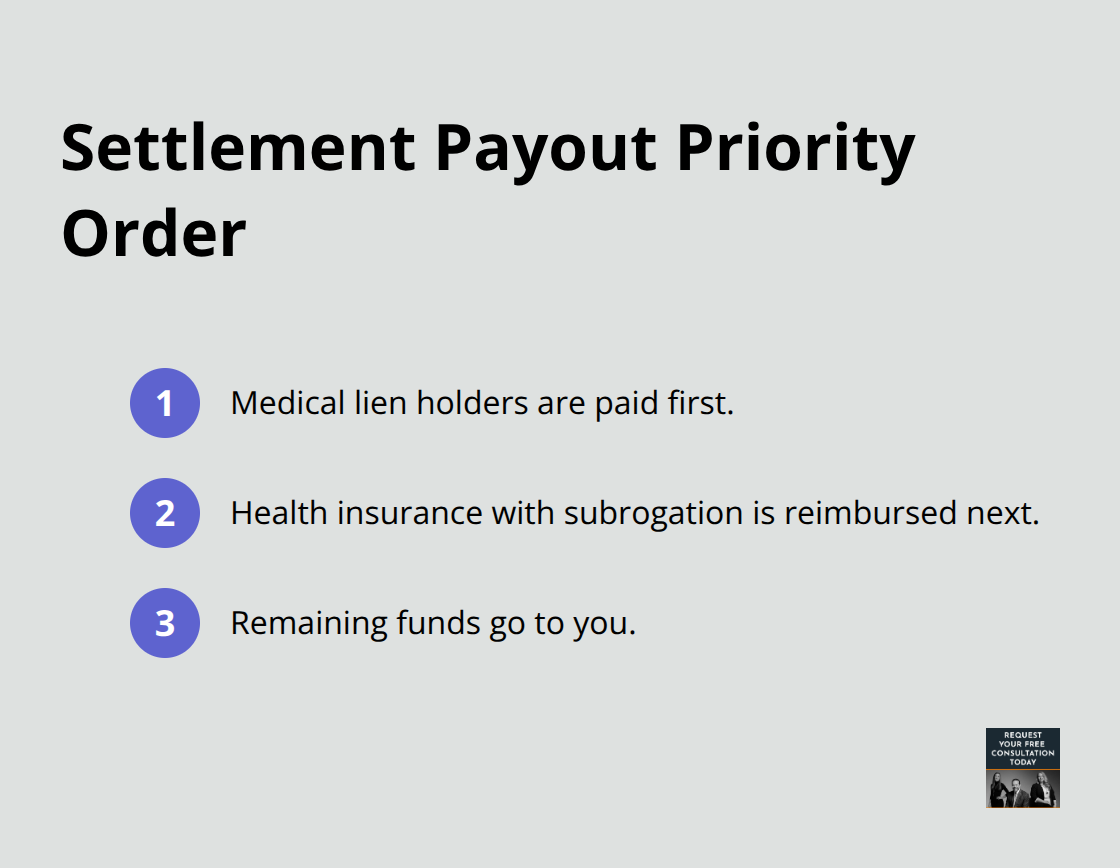

When your settlement finally arrives, the priority order matters significantly. Medical lien holders get paid first from your settlement check, then health insurance companies if they have subrogation rights, then you receive the remainder.

Understand this priority before accepting any settlement offer because it determines your actual take-home amount. If your settlement is $50,000 but medical liens total $15,000 and health insurance subrogation is $8,000, you receive approximately $27,000 after those obligations are paid. Calculate these figures before negotiations conclude so you know whether an offer actually covers your needs. We at Schaar & Silva LLP can help direct you to medical lien services that protect your access to care while securing your financial recovery, ensuring bills don’t derail your treatment or your claim.

Final Thoughts

Protecting your medical bills after a Santa Cruz car accident requires action on multiple fronts. Start immediately by documenting every medical expense, requesting itemized bills from providers, and establishing medical liens before treatment escalates. Contact your medical providers within two weeks to discuss lien options and secure written cost estimates for ongoing care.

Injury protection Santa Cruz residents deserve goes beyond covering immediate medical bills-it means securing access to necessary treatment without financial panic, protecting your credit from collection agencies, and recovering the full value of your claim. The coordination between liability claims, MedPay, medical liens, and health insurance creates complexity that most accident victims navigate poorly alone, and missing even one of these tools costs you thousands in recoverable expenses.

We at Schaar & Silva LLP help Santa Cruz accident victims move through this process with confidence. Contact us for a free case review to understand your claim’s value and the steps needed to maximize your medical bill recovery.