You’ve received a settlement check after your car accident, and now you’re wondering: is auto accident settlement taxable?

The answer isn’t straightforward. Some settlement money is tax-free, while other portions may be subject to federal taxes. At Schaar & Silva LLP, we help accident victims understand exactly what they owe and what they keep.

This guide breaks down the tax rules so you know what to expect when filing your return.

What the IRS Actually Taxes in Your Settlement

The IRS Doesn’t Tax All Settlement Money Equally

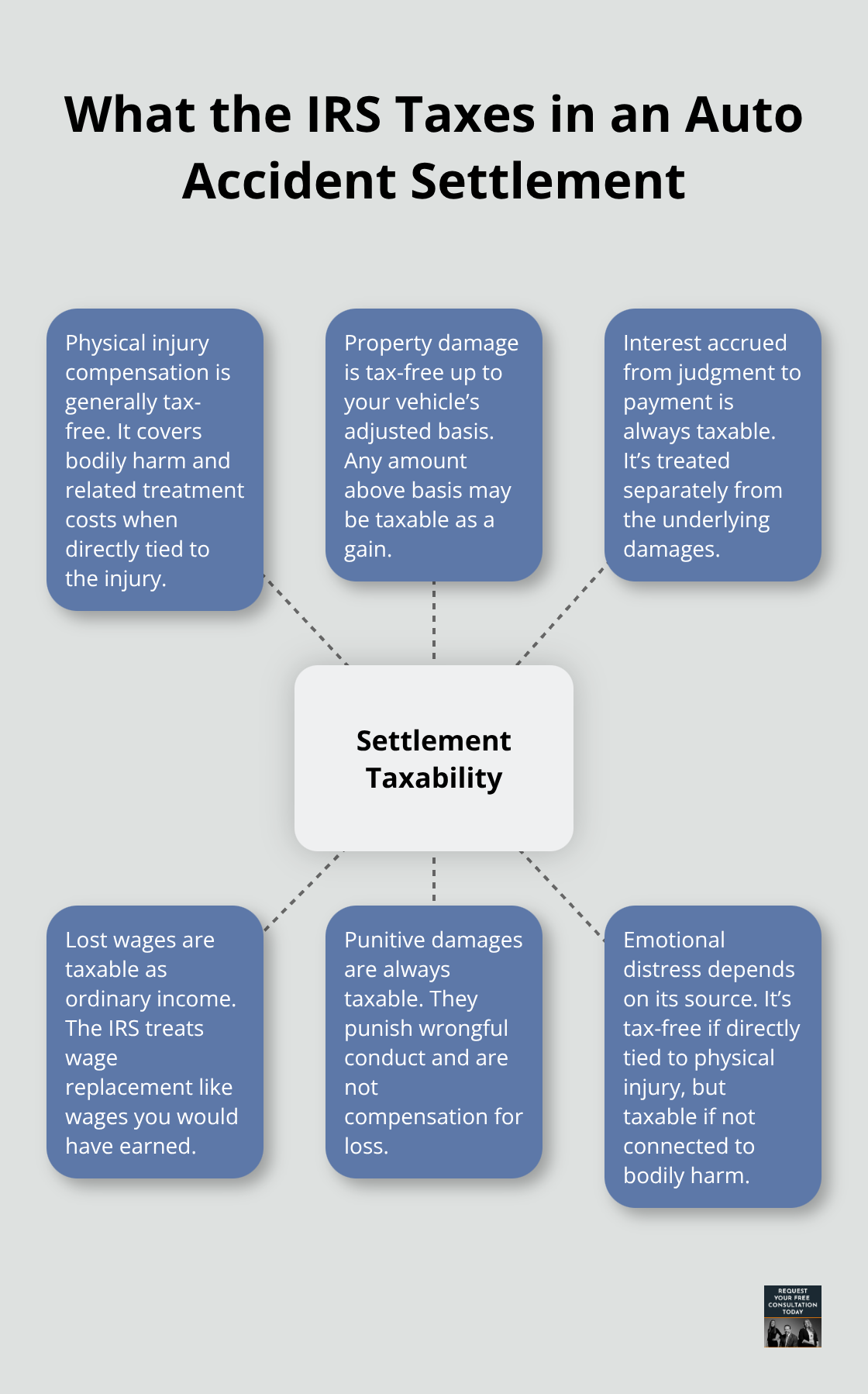

The IRS applies different tax rules to different parts of your settlement. Under Section 104 of the Internal Revenue Code, compensation for personal physical injuries or physical sickness remains tax-free. This rule forms the foundation of settlement taxation. However, the moment your settlement includes damages for anything other than physical injury-punitive damages, lost wages, or interest-those portions become taxable. The distinction matters enormously because it determines what you owe at tax time.

A settlement that looks like one large check often contains multiple components, each with different tax consequences. This is why vague settlement agreements create problems. If your agreement doesn’t clearly separate compensatory damages from punitive damages, the IRS will scrutinize the allocation.

Courts have ruled consistently that the nature of the damage, not what the settlement agreement labels it, determines taxability. For example, if you received a verdict for $1 million in compensatory damages and $3 million in punitive damages, then settled for $2 million on appeal, the IRS may treat 75 percent of that settlement as punitive unless your settlement language and appellate posture support a different allocation. This recharacterization happens frequently, and most settlement recipients don’t see it coming until they file their taxes.

Medical Bills and Property Damage Remain Tax-Free

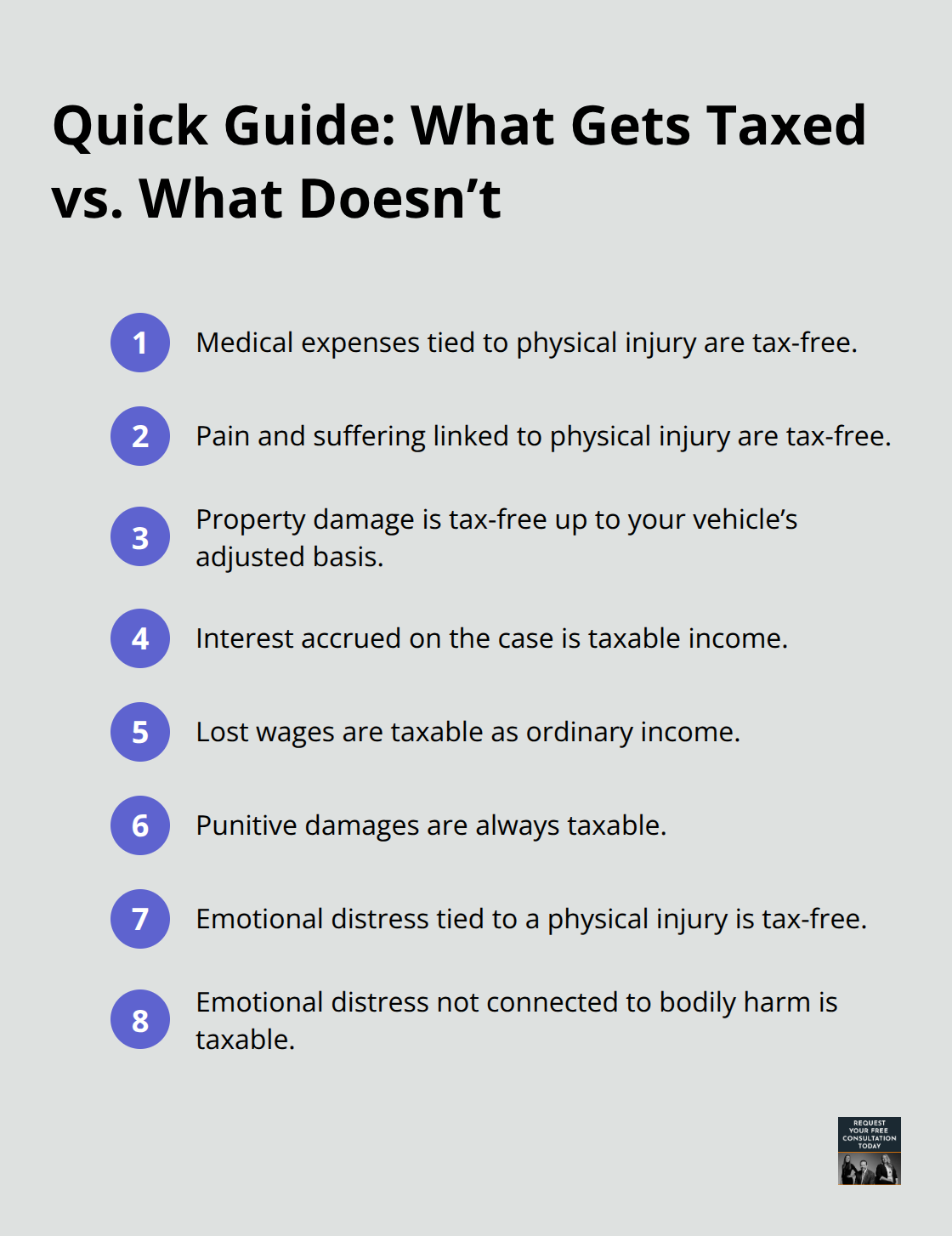

Medical expense reimbursements stay tax-free when they compensate for actual bills you paid. If your settlement allocates $15,000 for medical expenses, surgery, physical therapy, and hospital costs, that portion never gets reported as income. The same applies to property damage. If your car needed $8,000 in repairs and the settlement covers that amount, it’s not taxable because it restores what was lost, not creates new income.

Documentation makes the difference. Keep all medical bills, receipts, repair estimates, and invoices. When you can show the IRS exactly what you spent, defending the tax-free portion becomes straightforward. Property damage gets trickier only if the settlement exceeds your vehicle’s adjusted basis. If your car had an adjusted value of $12,000 and you received $15,000 for property damage, the excess $3,000 may be taxable as a gain.

Interest that accrues on any settlement from the judgment date to payment date is always taxable, completely separate from the underlying damages. Many residents overlook this. If your case took three years to resolve and $50,000 in interest accumulated, that $50,000 is taxable income regardless of how the settlement agreement characterizes the principal.

Lost Wages and Punitive Damages Always Become Taxable

Lost wages included in your settlement are taxable as ordinary income. This applies whether you lost income directly because of your injury or because you missed work during treatment and recovery. The IRS treats wage replacement the same way it treats wages you actually earned. If your settlement allocates $25,000 for lost income, you report it as taxable income.

Punitive damages present an even clearer tax problem. These damages punish the defendant for wrongful conduct, not compensate you for losses. The IRS taxes punitive damages at full rates with no exceptions. If a jury awarded $500,000 in punitive damages as part of your verdict, that amount is taxable even if you later settled for less. The allocation in your settlement agreement matters, but so does the original verdict. If the settlement language tries to reclassify punitive damages as compensatory to reduce your tax burden, the IRS looks past that language to the actual nature of the damages.

Emotional Distress: The Complication That Catches Most People Off Guard

Emotional distress creates the final complication in settlement taxation. Emotional distress damages tied directly to your physical injury are tax-free. If the accident caused back pain and anxiety related to that pain, and your settlement separately allocates damages for that distress, it’s excludable. Emotional distress unconnected to physical injury-like humiliation or reputational harm-is taxable.

The IRS wants clear evidence that the distress stems from the physical injury itself, not from other circumstances surrounding the accident. This aggressive IRS scrutiny means settlements involving emotional distress components require careful documentation and professional guidance. The way you allocate these damages in your settlement agreement directly affects your tax liability, which is why the next section on documentation and reporting becomes essential to protecting yourself.

What Gets Taxed and What Doesn’t

Physical Injury Compensation Stays Tax-Free

Physical injury compensation forms the tax-free foundation of your settlement, but only when the damages directly address your bodily harm. Section 104 protects compensation for medical expenses, surgery, physical therapy, hospital stays, and ongoing treatment related to your injury from taxation. Pain and suffering damages also remain tax-free when they stem directly from the physical injury itself.

If your settlement allocates $40,000 for medical bills and $20,000 for pain and suffering tied to your injury, both portions avoid taxation.

Documentation proves critical here. Keep every medical bill, receipt, prescription record, and therapy invoice. When the IRS questions your allocation, these records demonstrate exactly what you spent and why those amounts qualify as injury-related compensation.

Property Damage and Interest Require Careful Attention

Property damage stays tax-free up to your vehicle’s adjusted basis. If repairs cost $8,500 and your car’s adjusted value was $12,000, the repair reimbursement carries no tax consequence. However, if you received $15,000 for property damage on that same $12,000 vehicle, the excess $3,000 becomes taxable gain.

Interest accrued during your case represents a separate taxable component entirely. A three-year case that generated $45,000 in pre-judgment and post-judgment interest means $45,000 of taxable income, regardless of how your settlement agreement structures the principal amount.

Lost Wages and Punitive Damages Always Trigger Taxation

Lost wages included in your settlement are taxable as ordinary income, treated identically to wages you would have earned. A $30,000 allocation for lost income during your recovery period gets reported as taxable income on your tax return.

Punitive damages present an absolute tax certainty: they are always taxable with no exceptions. If a jury awarded $500,000 in punitive damages and you later settled for $2 million total, the IRS will scrutinize how much of that settlement represents punitive versus compensatory damages. Courts have consistently ruled that the original verdict shapes the tax treatment, meaning settlement language alone cannot reclassify punitive damages as compensatory to reduce your tax burden.

Emotional Distress: The Gray Zone Most People Miss

Emotional distress creates the gray zone that catches most Santa Cruz accident victims unprepared. Emotional distress damages directly tied to your physical injury are tax-free, but emotional distress unconnected to bodily harm is taxable. If anxiety stemmed from back pain caused by the accident, that distress damage is excludable. If distress arose from humiliation, loss of reputation, or other non-physical sources, it becomes taxable income.

The IRS demands clear evidence linking the emotional harm to the physical injury itself, which means your settlement agreement must explicitly separate these components. Vague allocations invite aggressive IRS scrutiny and potential reclassification of portions you believed were tax-free. Understanding which damages fall into each category sets the stage for the documentation and reporting steps that protect you when filing your taxes.

Protecting Your Settlement With Proper Documentation and Tax Reporting

Organize Your Records From Day One

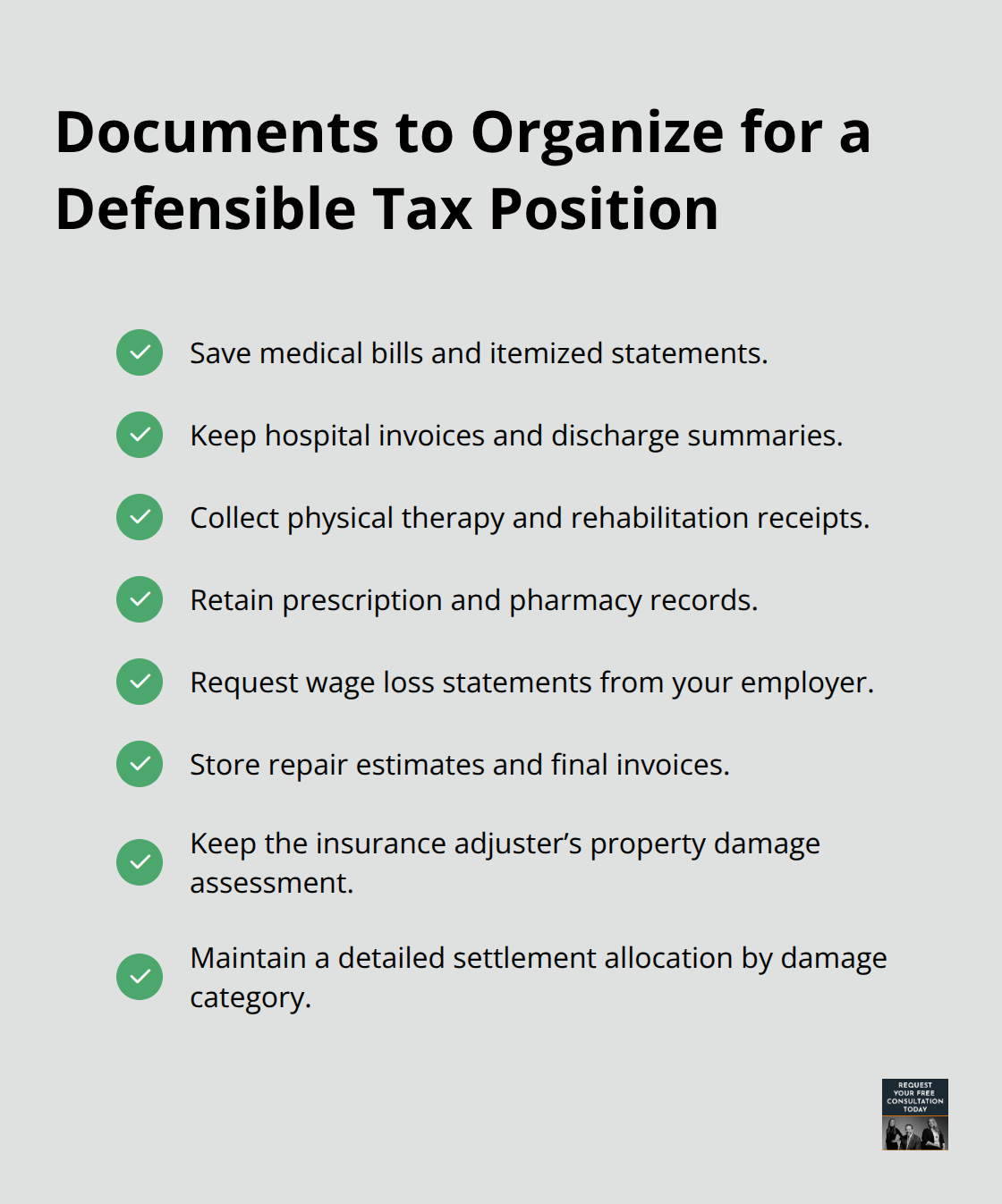

Detailed records from the moment of your accident separate those who face surprise tax bills from those who navigate settlement taxes smoothly. Collect and organize documents immediately: medical bills, hospital invoices, physical therapy receipts, prescription records, wage loss statements from your employer, repair estimates, and the insurance adjuster’s property damage assessment. These documents form the backbone of your tax defense. When the IRS questions your allocation between tax-free medical expenses and taxable lost wages, you need proof that shows exactly what you spent on each category. Store these records digitally and physically in separate folders labeled by damage type.

Many Santa Cruz residents assume their settlement agreement alone protects them from IRS scrutiny, but the agency looks beyond the agreement to your actual expenses. If your settlement allocates $35,000 for medical care, you must produce bills totaling at least that amount. Without comprehensive documentation, the IRS can reclassify portions of your settlement as taxable income, resulting in unexpected tax liability plus penalties.

Understand Your 1099 Reporting Obligations

Reporting requirements depend entirely on which portions of your settlement are taxable. The IRS will send you Form 1099-MISC if your settlement includes taxable components like lost wages, punitive damages, or interest. This form arrives in January following the settlement year and triggers your obligation to report that income on your federal tax return. Non-taxable portions like medical expense reimbursements and pain and suffering tied to physical injury do not appear on any tax form.

The critical step happens before you receive the 1099: ensure your settlement agreement explicitly allocates each component by category. Language stating medical expenses total $20,000, lost wages total $15,000, and punitive damages total $5,000 gives you and the IRS a clear roadmap. Vague language like “settlement amount $40,000” with no breakdown invites the IRS to make its own allocation, which rarely favors the taxpayer.

Work With a Tax Professional Before Finalizing Your Settlement

A tax advisor can review your allocation, identify which portions trigger 1099 reporting, and calculate your actual tax liability. This coordination between your legal team and tax advisor ensures the settlement agreement language aligns with tax law requirements and protects you when filing your return. A tax professional working alongside your attorney throughout settlement negotiations structures agreements that minimize your tax burden while remaining defensible to the IRS.

Final Thoughts

The question of whether an auto accident settlement is taxable has no single answer because your settlement likely contains multiple components, each with different tax consequences. Medical expenses and pain and suffering tied to your physical injury remain tax-free, while lost wages, punitive damages, and accrued interest become taxable income. The difference between what you keep and what you owe often comes down to how clearly your settlement agreement allocates each damage category.

A vague settlement invites IRS scrutiny and potential reclassification that works against you, but a detailed allocation with supporting documentation protects you when filing your return. Your attorney and a tax advisor working together can structure your settlement to minimize tax liability while remaining defensible to the IRS. This coordination happens before you sign the settlement agreement, not after you receive the check.

Gather your medical bills, repair estimates, wage loss statements, and settlement agreement, then schedule a consultation with a tax professional before finalizing your settlement. If you haven’t yet retained legal representation, contact Schaar & Silva LLP to discuss your case and coordinate with a tax advisor who can answer your specific questions about settlement taxation and reporting requirements.