Car accidents in Santa Cruz County often leave drivers facing thousands in vehicle damage costs. Insurance companies frequently offer settlements that fall far below actual repair expenses and vehicle value.

We at Schaar & Silva LLP see how these lowball offers impact local families daily. A skilled vehicle damage lawyer can fight for the full compensation you deserve after your accident.

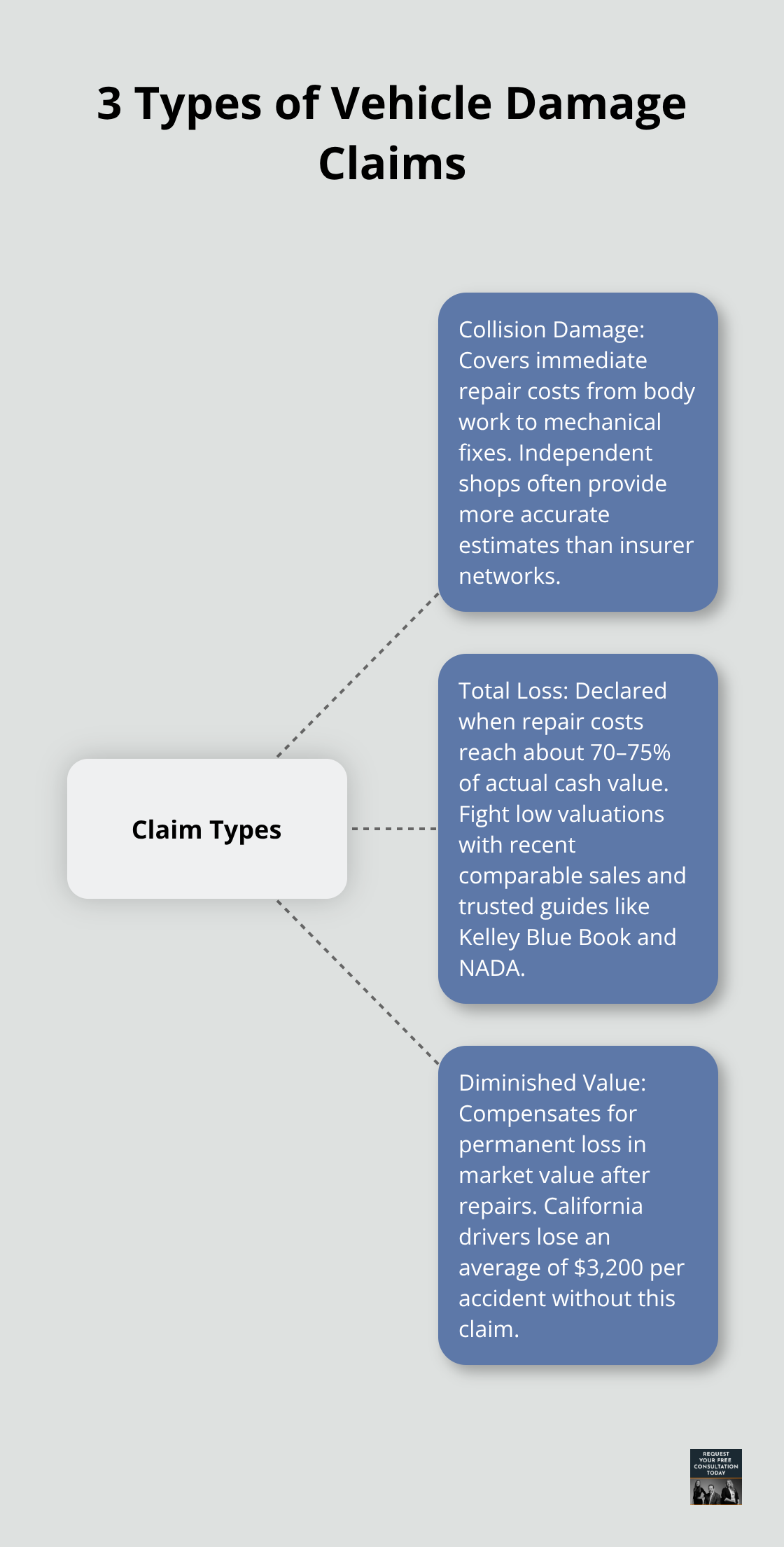

Types of Vehicle Damage Claims

Vehicle damage claims fall into three distinct categories, each requiring different approaches to maximize compensation. Collision damage represents the most straightforward claim type, covering immediate repair costs from body work to mechanical fixes. California drivers face average repair costs of $4,500 per collision, yet insurance adjusters routinely undervalue estimates by 15-20% according to National Association of Insurance Commissioners data. Property damage liability minimums in California remain at just $5,000, creating massive coverage gaps when repair bills exceed this amount.

Collision Damage and Repair Costs

Insurance companies calculate collision damage through their preferred repair networks, often selecting the lowest bidder rather than quality shops. These arrangements benefit insurers but leave you with substandard repairs and potential safety issues. Independent body shops typically provide more accurate estimates that reflect true repair costs. California law allows you to choose your repair facility, though adjusters may pressure you toward their network partners (who often cut corners to maintain insurance contracts).

Total Loss and Fair Market Value

Insurance companies declare total loss when repair costs reach 70-75% of your vehicle’s actual cash value, though this threshold varies by insurer. The problem lies in how companies calculate fair market value. Adjusters often use outdated databases or ignore recent comparable sales, reducing payouts by thousands. Kelly Blue Book and NADA Guides provide more accurate valuations, but you must fight for these higher assessments. California’s three-year statute of limitations gives you time to challenge unfair total loss settlements.

Diminished Value Claims

Diminished value claims address the permanent loss in vehicle worth after repairs, even when restoration appears complete. This hidden damage costs California drivers an average of $3,200 per accident according to Automotive News research. Insurance companies rarely mention diminished value rights, hoping you’ll overlook this significant compensation category. The calculation requires professional appraisal comparing pre-accident value to current market worth. Most drivers accept initial settlements without understanding how insurance companies manipulate these complex valuation processes.

How Insurance Companies Handle Vehicle Damage Claims

Insurance adjusters arrive at accident scenes within hours, armed with tablets and damage assessment apps that minimize payouts from first contact. These field adjusters work under strict quotas that require them to close cases quickly and cheaply, often taking photographs from angles that conceal the worst impacts. State Farm and Allstate train adjusters to use specific language patterns that subtly shift blame toward drivers, with recorded statements that become weapons against your claim later. The initial damage estimate typically covers only visible surface damage while it ignores underlying structural problems that emerge during actual repairs.

The 72-Hour Settlement Push

Insurance companies launch aggressive settlement campaigns within 72 hours of accidents because they know that shocked victims often accept lowball offers before they understand their true losses. Progressive and Geico representatives contact Santa Cruz County drivers with same-day settlement offers that average 40-60% below actual damage costs (according to California Department of Insurance complaints data). These quick settlements include release forms that prevent future claims for hidden damage or diminished value. The pressure tactics include phrases like “limited time offer” and “avoid lengthy legal processes” that create false urgency. Smart drivers refuse these initial offers and demand independent damage assessments from certified appraisers who find an average of $2,800 in additional damage that insurance adjusters miss.

Digital Manipulation and Valuation Games

Modern insurance companies use artificial intelligence and photo analysis software to automatically reduce claim values before human review begins. Farmers Insurance and Liberty Mutual deploy computer programs that flag claims for denial based on damage patterns, accident locations, and driver profiles.

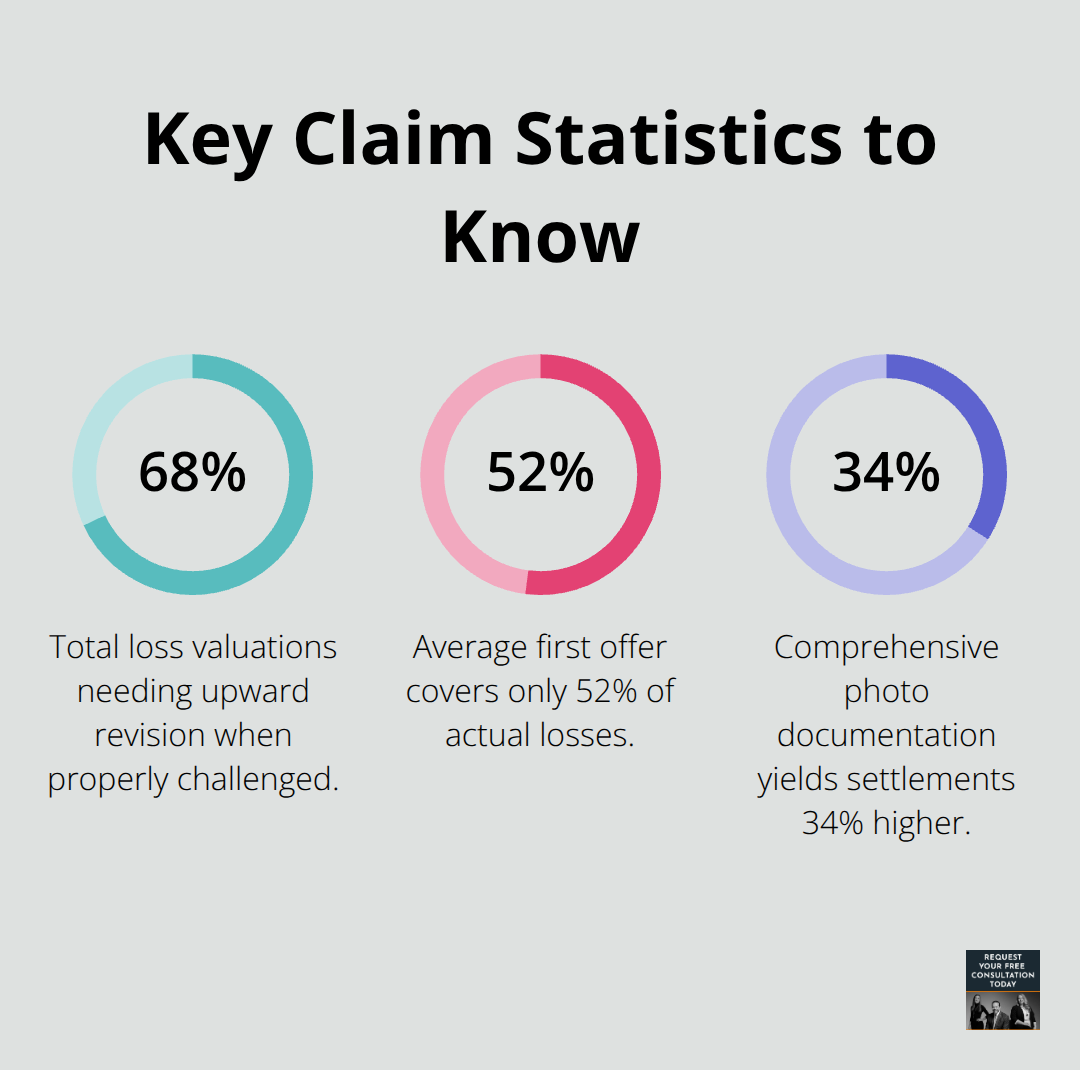

These systems systematically undervalue vehicles when they use specific formulas to determine vehicle values that often shortchange accident victims, cherry-pick low-mileage comparables from distant markets, and ignore recent sales of similar vehicles. The National Association of Insurance Commissioners found that 68% of total loss valuations require upward revision when challenged with proper market research and professional appraisals.

When Settlement Offers Fall Short

Insurance companies present initial offers as final settlements, but these amounts rarely reflect true damage costs or legal compensation standards. The average first offer covers just 52% of actual losses according to Insurance Research Council data, leaving thousands in unclaimed compensation on the table. Companies count on driver acceptance of these inadequate amounts to protect their profit margins. When you reject lowball offers, adjusters often claim policy limits or dispute liability to justify their positions. This resistance signals the need for legal intervention to secure fair compensation through proper documentation and negotiation tactics.

Legal Steps to Maximize Your Vehicle Damage Compensation

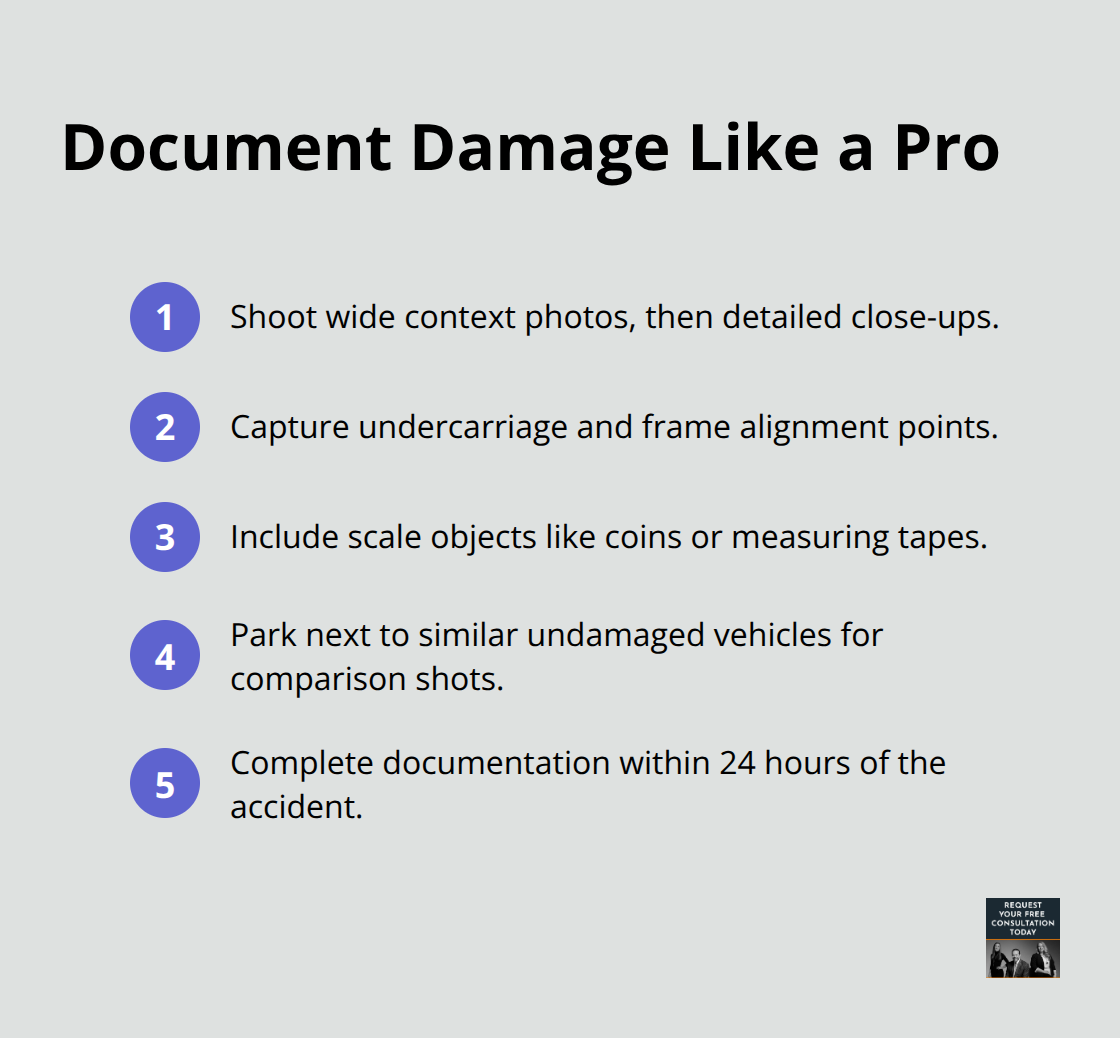

Professional photography becomes your strongest weapon against insurance company manipulation. Take close-up shots of all damage from multiple angles, including areas adjusters typically ignore like undercarriage components and frame alignment points. California Department of Motor Vehicles data shows that drivers who provide comprehensive photo documentation receive settlements 34% higher than those who rely solely on adjuster photos. Document damage within 24 hours of your accident, before weather or movement can worsen visible problems.

Include reference objects like coins or measuring tapes to demonstrate scale, and photograph your vehicle next to similar undamaged models to highlight impact severity.

Document Your Damage Properly

Insurance companies manipulate evidence through selective photography that minimizes visible damage. You must create your own comprehensive damage record that captures every impact point, scratch, and structural problem. Take wide-angle shots that show the accident scene context, then move to detailed close-ups of each damaged component. Focus on areas where metal has bent, paint has chipped, or panels have shifted out of alignment. Weather conditions can obscure damage within hours, so complete your documentation immediately after the accident occurs.

Obtain Independent Professional Appraisals

Insurance companies hate independent appraisals because certified automotive appraisers find an average of $4,200 in additional damage that company adjusters miss or minimize. American Society of Appraisers members charge $400-600 for comprehensive vehicle assessments, but this investment typically returns $3,000-8,000 in additional compensation (according to National Association of Public Insurance Adjusters research). Schedule your independent appraisal before you accept any settlement offer, as insurance companies use signed agreements to block future damage claims. Professional appraisers identify hidden structural damage, verify proper repair procedures, and calculate fair compensation for damages that insurance companies routinely underestimate by 40-60%.

Challenge Insurance Company Valuations

Insurance adjusters use computer programs that automatically reduce vehicle values through selective comparable sales and outdated market data. You can challenge these valuations with recent sales records from AutoTrader, Cars.com, and local dealership listings that show higher market values for similar vehicles. Print documentation of comparable vehicles with similar mileage, condition, and features that sold within the past 30 days in your geographic area. Present this evidence to adjusters with a formal demand letter that requires them to justify their lower valuation methods.

File a Lawsuit When Negotiations Fail

California Civil Code Section 3333 requires insurance companies to pay actual cash value plus reasonable rental costs, but companies violate these requirements in 43% of total loss claims according to California Department of Insurance violation reports. File a lawsuit when companies refuse fair payment after you present proper documentation and independent appraisals. Superior Court of California requires insurance companies to pay attorney fees when they unreasonably deny valid claims, which makes legal action financially viable even for moderate damage amounts. Litigation discovery often uncovers company policies that prioritize profit over fair claim resolution, which provides leverage for substantially higher settlements.

Final Thoughts

Contact a vehicle damage lawyer immediately when insurance companies offer settlements below your actual losses or refuse to negotiate fair compensation. We at Schaar & Silva LLP see insurance companies deny valid claims in 43% of cases, hoping drivers will accept inadequate payments without legal challenge. Legal representation increases settlement values by an average of 3.5 times according to Insurance Research Council data.

Attorneys force insurance companies to follow California law rather than internal profit guidelines that prioritize company earnings over fair compensation. Insurance companies take legal representation seriously because attorneys understand valuation manipulation tactics and statutory requirements that companies routinely violate. Our team evaluates damage extent and secures fair valuations for your losses while we connect you with medical lien services for bill assistance.

Start your vehicle damage claim by documenting all damage thoroughly and rejecting lowball settlement offers. Document every impact point and structural problem before weather or movement can worsen visible damage. Contact Schaar & Silva LLP for a case evaluation that determines your claim’s true value and develops a strategy to secure full compensation from insurance companies that profit from underpaying Santa Cruz County drivers (who often accept inadequate settlements without understanding their legal rights).