Car accidents with underinsured drivers can leave victims facing significant financial burdens. Underinsured motorist coverage in California provides crucial protection against these risks.

At Schaar & Silva LLP, we’ve seen firsthand how this coverage can make a substantial difference for accident victims. This post explores the ins and outs of underinsured motorist coverage in California, helping you understand its importance and how to navigate claims effectively.

What Is Underinsured Motorist Coverage?

The Basics of Underinsured Motorist Coverage

Underinsured motorist coverage protects you when an accident involves a driver who lacks sufficient insurance to cover all your damages. This type of auto insurance is particularly important in California, where many drivers carry only minimal insurance.

Your own policy steps in to cover the difference between the at-fault driver’s policy limit and your actual damages. For instance, if you incur $50,000 in medical bills and lost wages, but the at-fault driver only has $15,000 in coverage, your underinsured motorist coverage can pay the remaining $35,000 (subject to your policy limits).

Underinsured vs. Uninsured Motorist Coverage

While often bundled together, these coverages serve different purposes:

- Uninsured motorist coverage: Protects you when you’re hit by a driver with no insurance at all.

- Underinsured coverage: Applies when the at-fault driver has some insurance, but not enough to cover all your damages.

California’s Legal Requirements

In California, insurance companies must offer underinsured motorist coverage, but drivers can opt to waive it in writing. The state mandates minimum coverage of $15,000 per person and $30,000 per accident for bodily injury. However, these minimums often fall short in serious accidents.

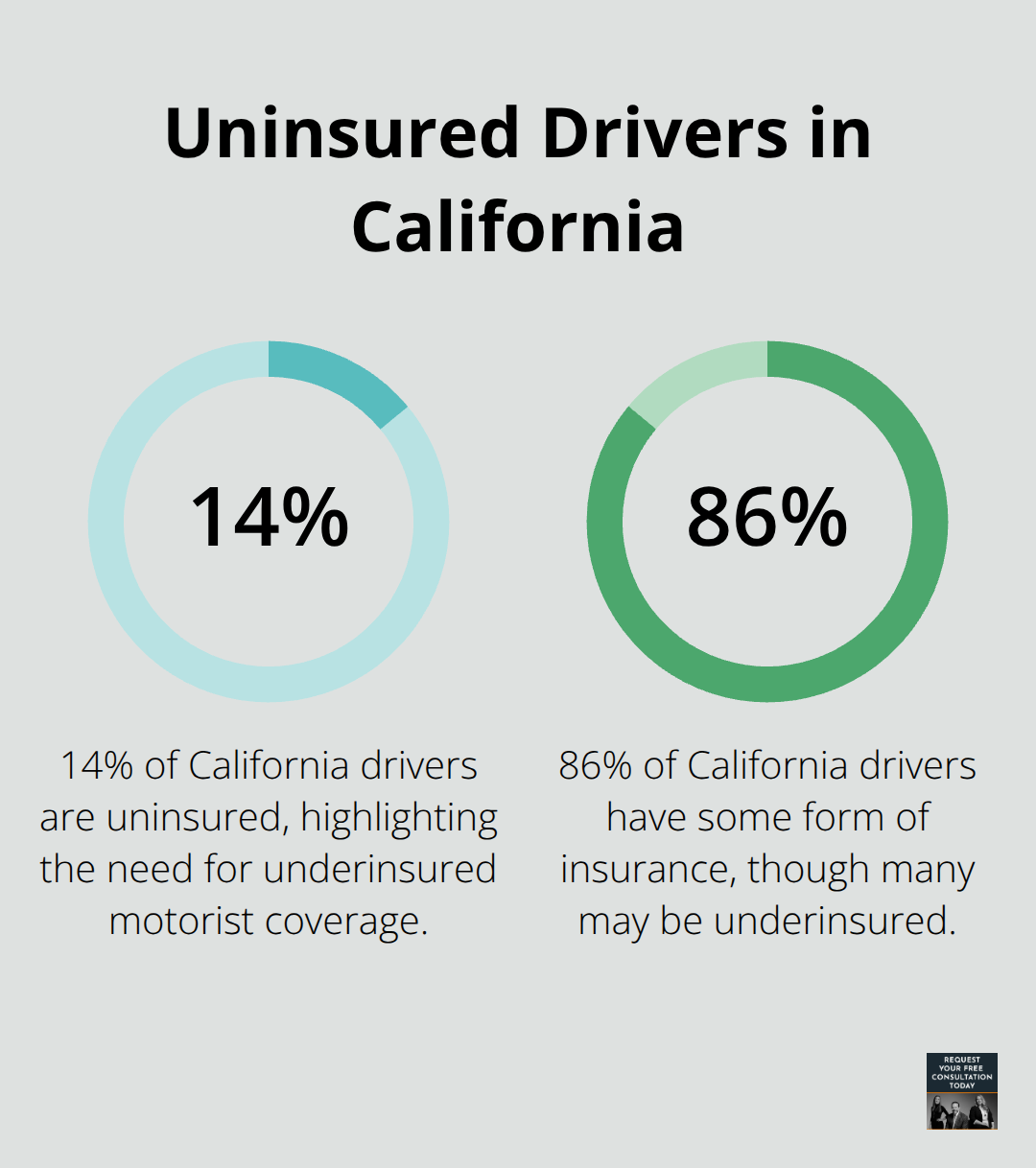

The California Department of Insurance reports that over 14% of California drivers are uninsured, and many more are underinsured. This statistic highlights the need for adequate coverage to protect yourself.

Why Underinsured Motorist Coverage Matters

- Financial Protection: It safeguards you from out-of-pocket expenses when the at-fault driver’s insurance is insufficient.

- Peace of Mind: Knowing you have this coverage can alleviate stress after an accident.

- Broader Coverage: It can cover not just you, but also family members (in certain circumstances).

Choosing the Right Coverage

When selecting underinsured motorist coverage:

- Consider Your Assets: Higher limits may be necessary if you have significant assets to protect.

- Evaluate Your Risk: If you frequently drive in areas with high rates of uninsured or underinsured drivers, more coverage might be wise.

- Review Your Health Insurance: If your health insurance has high deductibles or limited coverage, robust underinsured motorist coverage becomes even more important.

Understanding underinsured motorist coverage is just the first step. Next, we’ll explore the specific benefits this coverage provides and how it can protect you financially in the event of an accident with an underinsured driver.

How Does Underinsured Motorist Coverage Protect You?

Financial Protection Beyond Basic Limits

Underinsured motorist coverage acts as a powerful shield against financial hardship after an accident. This protection activates when the at-fault driver’s insurance fails to cover your damages fully. In California, the minimum liability coverage required is $15,000 per person and $30,000 per accident. These limits often prove inadequate in serious accidents.

Your underinsured motorist policy bridges this gap. For instance, if you sustain $50,000 in damages and the at-fault driver only has $15,000 in coverage, your policy can cover the remaining $35,000 (subject to your policy limits).

The California Department of Insurance reports that accident-related medical costs often exceed $50,000. Without adequate coverage, you could face substantial out-of-pocket expenses. Underinsured motorist coverage prevents this financial burden from falling on your shoulders.

Comprehensive Coverage for Various Expenses

Underinsured motorist coverage extends beyond just medical bills. It can cover lost wages if injuries from the accident prevent you from working. This aspect of coverage proves particularly valuable for self-employed individuals or those without robust disability insurance.

Moreover, this coverage can help with ongoing medical treatments and rehabilitation costs. National Highway Traffic Safety Administration (NHTSA) data shows that severe injuries from car accidents often require long-term care, which can quickly deplete standard insurance limits.

Compensation for Non-Economic Damages

One often overlooked benefit of underinsured motorist coverage is its potential to compensate for pain and suffering. While it’s challenging to put a price on these non-economic damages, they form a significant part of many accident claims.

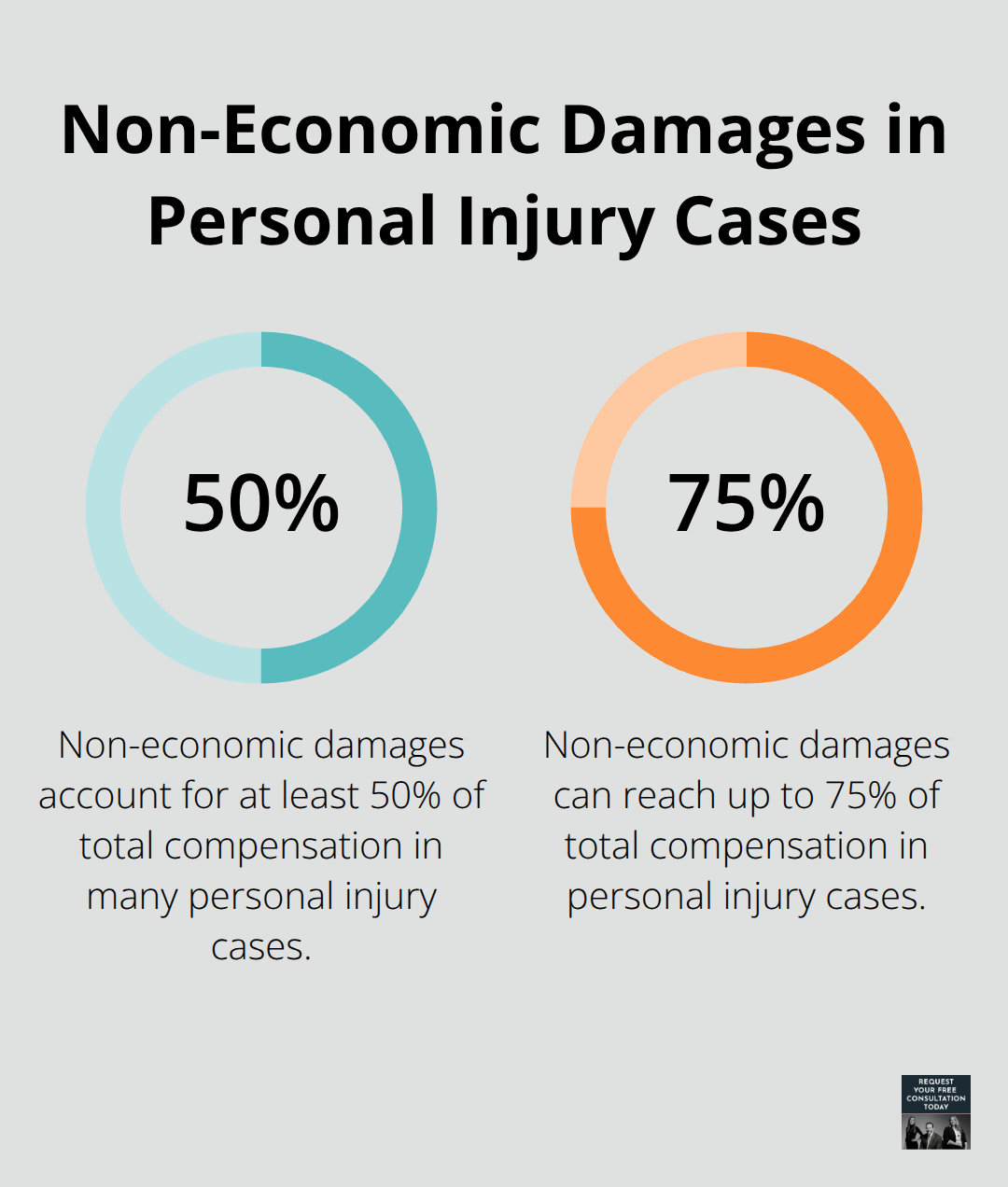

The Insurance Research Council found that non-economic damages often account for 50% to 75% of total compensation in personal injury cases (a substantial portion of the overall claim). Underinsured motorist coverage ensures you’re not left without recourse for these intangible but very real consequences of an accident.

Protection for Family Members

Underinsured motorist coverage doesn’t just protect you; it can also cover family members in certain circumstances. This extended protection (which typically includes household members) adds an extra layer of security for your loved ones.

Coverage in Various Scenarios

Your underinsured motorist coverage can protect you in various situations, not just when you’re driving. It may apply if you’re:

- A passenger in someone else’s vehicle

- Hit by a car while walking or cycling

- Involved in a hit-and-run accident (where the at-fault driver’s insurance status is unknown)

Understanding the benefits of underinsured motorist coverage is essential, but knowing how to file a claim is equally important. The next section will guide you through the process of filing an underinsured motorist claim in California, ensuring you’re well-prepared to protect your rights and interests.

How to File an Underinsured Motorist Claim in California

Immediate Steps After an Accident

After an accident with an underinsured driver, prioritize safety. Once safe, collect as much information as possible at the scene:

- The other driver’s insurance information

- Photos of the accident scene and vehicle damage

- Contact details of any witnesses

Report the accident to the police and your insurance company promptly. The California Highway Patrol recommends filing a report within 24 hours for accidents resulting in injuries or significant property damage.

Essential Documentation

To file a successful underinsured motorist claim, you’ll need comprehensive documentation:

- Medical records and bills related to your injuries

- Proof of lost wages if you missed work due to the accident

- Repair estimates or bills for vehicle damage

- A copy of the police report

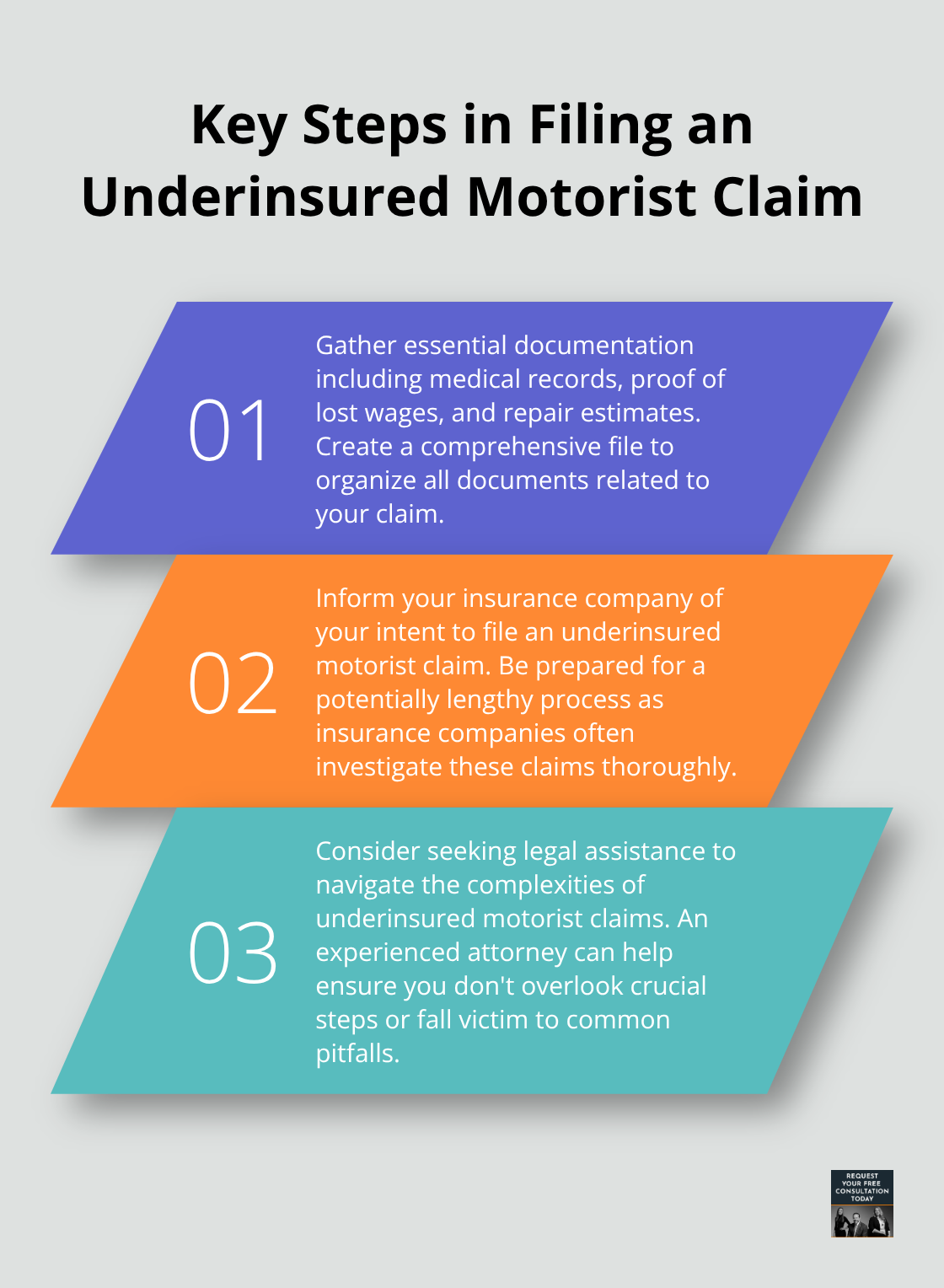

Create a file to organize all documents related to your claim (as suggested by the National Association of Insurance Commissioners).

Time Limits for Filing

In California, you typically have two years from the date of the accident to file an underinsured motorist claim. However, this timeline can be complex. The clock usually starts when you “exhaust” the at-fault driver’s policy limits.

The California Department of Insurance cautions that failure to file within the statute of limitations can result in the loss of your right to compensation. Consult with an attorney as soon as possible after the accident to avoid missing critical deadlines.

Navigating the Claims Process

Once you’ve gathered your documentation, inform your insurance company of your intent to file an underinsured motorist claim. Prepare for a potentially lengthy process, as insurance companies often investigate these claims thoroughly.

During this process, you may need to:

- Provide a recorded statement (consult an attorney before doing so)

- Undergo an independent medical examination

- Participate in negotiations with the insurance adjuster

Insurance companies aim to minimize payouts and may use tactics to devalue your claim. This is where experienced legal representation proves invaluable.

Legal Assistance

An attorney can help you navigate the complexities of underinsured motorist claims. They ensure you don’t overlook any crucial steps or fall victim to common pitfalls. If you’re in Santa Cruz County, consider reaching out to Schaar & Silva LLP for guidance through this process.

To file a compensation claim for a car accident in Santa Cruz, learn about the steps, tips, and local resources that can help streamline your claim process.

Final Thoughts

Underinsured motorist coverage in California protects drivers from financial hardship when accidents involve inadequately insured motorists. This protection becomes essential with many California drivers carrying only minimum coverage or no insurance at all. Drivers should consider factors beyond state-mandated minimums when selecting coverage limits, including assets, potential medical costs, and driving frequency.

The complexities of underinsured motorist claims can challenge those dealing with injuries and property damage. Professional legal assistance proves invaluable in these situations. Schaar & Silva LLP offers support throughout the claims process for auto accident cases in Santa Cruz County.

Underinsured motorist coverage in California provides comprehensive financial protection on the road. This coverage safeguards against potentially devastating consequences of accidents involving underinsured drivers. Proper understanding of its importance and seeking legal guidance when needed can help drivers navigate these challenging situations effectively.